A Primer on Tokenized Securities

Level 3 - Virgin DeFi Analyst

Welcome Avatar!

The New York Stock Exchange (“NYSE”) formed its roots in 1972 when brokers in New York formalized rules for securities trading. By the mid-1800s, New York City began growing as a financial center and Wall Street began serving financing needs of railroads, banks and insurers.

Today, the NYSE is central to how investors discover prices for widely held stocks. The NYSE is registered with the SEC under Section 6 of the Securities Exchange Act of 1934 which contains the exchange’s regulatory obligations and oversight. The NYSE’s closing auction is the largest liquidity event in the U.S. equity market.

The NYSE just announced that it is building a 24/7 blockchain-based venue for tokenized securities.

In today’s post we will provide a primer on tokenized securities.

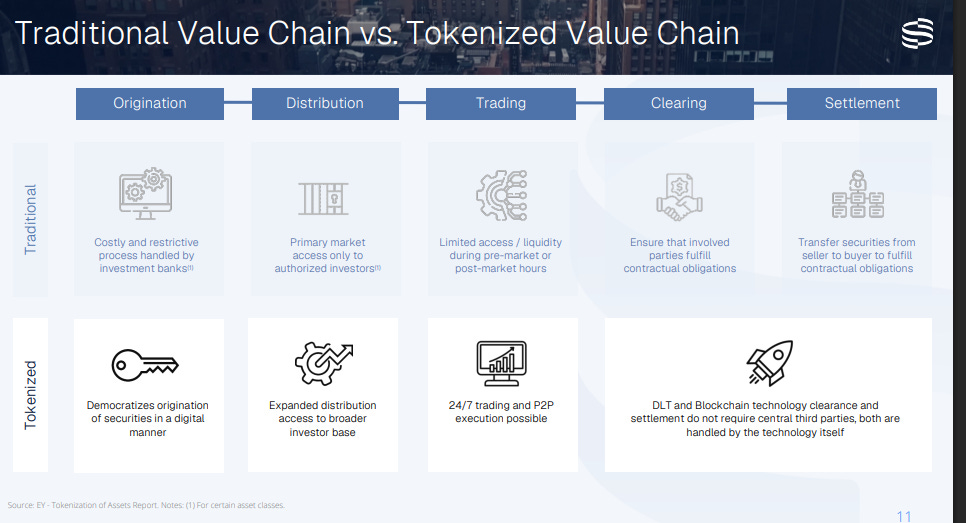

What are tokenized equities and securities?

Tokenized securities are traditional financial instruments (like shares or bonds) whose ownership is recorded on a blockchain via digital tokens. Owning a tokenized equity means you hold a blockchain-based token that confers the same rights as a share of stock (including dividends and voting) just as if you held a paper certificate or an entry in a broker’s database.

Tokenization doesn’t change the nature of the asset! A stock is still a stock. It changes how that asset is represented and transferred.

The concept of tokenized securities is not new. In the 2017 cycle several companies tried to do security tokens that were backed by equity or debt. The hype fizzled out due to regulatory complexity and a lack of liquidity.

Some of you may remember that exchanges like Binance and FTX offered tokenized stocks like Tesla that mirrored stock prices (held via a custodian) to let crypto traders get equity exposure. Due to compliance issues these operations were shut down.

In 2023, Blackrock CEO Larry Fink famously said that tokenization would be the next generation for markets.

Now, with the announcement of NYSE’s new venue, even the U.S. government is becoming involved. The Federal Reserve and SEC have observed trials of tokenized treasury bonds and stock settlement.

Why do tokenized equities matter?

The Big Idea with tokenized securities is that it can modernize securities infrastructure. Tokenized represent tangible value onchain that goes beyond tokens. The key benefits include

Around the clock trading and global access

Fractional ownership since tokens allow splitting an asset into tiny pieces

Auditability. Blockchains only allow for new records to be added, which reduces fraud/errors in the transaction trail

Smart contracts can bake compliance rules into the securities and make operations like dividend distributions entirely programmatic

Institutions have been experimenting with tokenized securities in recent years. Blackrock launched BUIDL which we’ve covered on DEFi Ed. KKR tokenized a portion of a $4B healthcare fund . Hamilton Lane also tokenized segments of its funds.

State of play & key players

Technically speaking, there are $350 billion of assets that have been tokenized. However, 90% of that is stablecoins (tokenized cash). ~$35 billion is RWAs ranging from government bonds to equities to investment funds. This is a tiny fraction of global securities markets, but we are still extremely early. The NYSE has a 200 year head start!

Thus far, fixed income tokens have achieved the most adoption. Specifically, tokenized US T-Bills and Bonds which have people looking for safe yields. Tokenized puiblic equities have seene fewer major developments. Growth stalled through the 2022 bear market, before inflecting sharply in 2023 and going near parabolic through 2024 and 2025.

There are a few key players you’ll want to watch.

Securitize

Securitize operates a FINRA-registered broker dealer and alternative trading system (“ATS”), hosting trading of tokenized securities like private company stocks, tokenized fund interests and tokenized bonds. Securitize has worked on high profile issuances including the aforementioned funds by KKR and Hamilton Lane. These branded onboardings have helped bring more credibility to the space.

Securitize is expected to go public via SPAC in 2026 ($CEPT).

Figure

Figure has orignated over $20B in loans on public blockchains. It launched an Onchain Public Equity Network (“OPEN”) that allows companies to list equities natively on blockchains. The key difference here is native listing rather than tokenizing existing equities via proxy. Figured has received FINRA approval to operate its own ATS and it will be the first issuer on OPEN by listing its own stock as a token. Figure’s consumer loan marketplace volume was $2.705B in Q4 2025 (up 131% YoY from Q4 2024).

TradFi Institutions

Hate it or love it, TradFi is a necessary participant in the tokenization process. TradFi institutions are the gatekeepers to capital markets.

Goldman Sachs and BNY Mellon launched digital tokens representing shares in money market funds on BNY’s LiquidityDirect, with ownership recorded on Goldman’s blockchain. Even though these are fund shares (not common stock), they matter because MMF shares are widely used for cash management and collateral.

Franklin Templeton’s BENJI product tokenizes shares of its U.S. government money market fund (FOBXX) and supports onchain subscriptions and transfers.

We will dive deeper on key players in Thursday’s Deep Dive Report.

Biggest challenges

Progress is undeniable, but tokenized securities will have to overcome major hurdles to reach mass adoption.

Key challenges include:

Regulations and legal uncertainty: This point is relatively well understood, and the regulatory framework is still evolving (and under active discussions).

Pilot programs e.g. the DTC tokenization scheme recently approved by the SEC maintain a distinction between the Official Records of Ownership and the state of the blockchain ledger. Entitlements are maintained as offchain records, transfers onchain are not irrevocable, and the DTC has a “root wallet” / master key which allows it to arbitrarily rewrite the blockchain state (convert/transfer/mint/burn any token without having the permission of the wallet owner or access to its private key). Many tokenization models are either a wrapped asset or a parallel ledger system. It’s too early to be certain what legal frameworks would apply where the blockchain record actually determined ownership. The SEC has repeatedly stated that “tokenized securities are still securities”, meaning putting a stock on a blockchain does not exempt it from compliance with securities laws. This came to the forefront when unregulated venues tried offering tokenized stocks. Regulatory skepticism extends to concerns about custody and market stability.

Market development: tokenized securities are useless if no one uses them. 24/7 trading isn’t that valuable without price discovery. A pool of active issuers ring fenced for accredited investors isn’t scalable. Liquidity would need to improve to make tokenized securities truly worthwhile. This may be acheived by formal, regulated tokenization of some high profile assets that onboards a critical mass of traders.

Public vs private markets: It’s worth noting the different incentives for public and private assets in tokenization. In public equities, trading is already electronic, efficient, and highly liquid. For large cap stocks the benefits of moving to a blockchain-based system (faster settlement, etc.) are incremental (nice to have but not revolutionary), since today’s system works well in terms of liquidity and price discovery. In private markets (like shares of a pre-IPO startup or interests in a real estate fund), trading is currently difficult or nonexistent. Tokenization offers a clear value proposition there by creating liquidity.

What’s next?

Despite major hurdles the trajectory for tokenized securities is quite positive. As crypto’s tech matures and regulations become more clear, the market will see further innovation. Given the “TAM” here, we anticipate significant investment into building out this crypto sector.

Specifically:

Broader institutional adoption: more banks and asset managers may look at tokenized offerings. Existing institutional users may look to increase the size of their offerings and products (going from $20 million bond to $200 million, for example).

Better crypto onboarding: As institutions and major players rub up against crypto’s own bottlenecks, we anticipate them eventually pushing for better onboarding and seamless integration with traditional financial infra so capital can move around more freely (and into their funds!)

Industry shaping impact: we’ve written for years that for DeFi to reshape the financial system, it needs to break out of its “closed loop” state that relies on speculation on valueless tokens for survival. This process is finally happening in a meaningful way. Trading productive assets of real companies will bring an entirely new wave of participants.

Pivotal moments will come from regulatory breakthroughs and successful “case studies” from TradFi institutions. While we are obviously somewhat biased, we believe the current state of tokenization is like early internet stock trading in the 90s - the humble beginning of a new normal.

Concluding thoughts

The building blocks for the future of financial markets are being laid right now. There will likely be a few cycles of trial and error before we get there, but the pieces are coming together.

In these early days, it’s important to stay informed and grounded. This primer has provided a data-driven overview but there is a lot more to explore. In Thursday’s Deep Dive Report for paid subscribers, we will go deeper on the specific projects and companies that could shape this next big chapter in the evolution of markets.

Paid subscribers get access to:

All of our past posts

Weekly Deep Dive Report

A comprehensive bi-weekly DeFi Roundup

Bi-weekly Q&A sessions with our team

Until next time..

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are opinions from an anonymous group of cartoon animals with Wall Street and Software backgrounds.

We now have a full course on crypto that will get you up to speed (Click Here)

Security: Our official views on how to store Crypto correctly (Click Here)

appreciate the overview... just one note ... "The New York Stock Exchange (“NYSE”) formed its roots in 1972 when brokers" ... 1792. plz fix!