Crypto's Wealthiest Company

Level 2 - Value Investor

Welcome Avatar!

Digital gold. Digital oil. Neither of these assets compare to the staggering profit generated by crypto’s wealthiest company - Tether.

Tether has evolved from purely the issuer of stablecoin USDT into an entity that more closely resembles a sovereign wealth fund. Over the last two years it has built a major capital allocation machine around its stablecoin business, with dedicated investments across finance, data, power, education, and an explicit venture arm. In April 2024, Tether formally reorganized around four main divisions: Finance, Data, Power, and Edu.

As a result, Tether has turned into one of the most fascinating corporate treasuries in the world with a sprawling 120+ company investment portfolio. In today’s post we peel back the onion on Tether the company. On Thursday’s deep dive we’ll dig into their biggest principal investments, reverse engineer their strategy and analyze the takeaways for our portfolios.

A Primer on Tether

Tether’s business model is relatively simple. It takes user deposits (dollars), issues digital tokens (USDT), and invests the underlying deposits in yield bearing assets, primarily U.S. Treasury bills.

Over recent years, stablecoin market caps have surged and interest rates have remained robust. This has turned Tether into one of the largest non-sovereign holders of U.S. debt in the world.

The company reported ~$13.7 billion in profit in 2024 and maintained profit north of $10 billion through 2025. With only 300 employees, Tether is likely the most profitable company per employee on the planet.

Tether’s profitability is driven almost entirely by net interest income. It earns yield on reserves (mainly U.S. Treasuries) and pays little or no yield to USDT holders. This creates a massive spread.

Billions of dollars in reserves * Treasury yields = multi-billion $ annual profit

This model has turned Tether into one of the most efficient profit generating entities in all of finance. It does not require a large workforce, a branch network, or heavy customer acquisition spend. USDT’s distribution is deeply embedded in the crypto ecosystem. Once USDT is issued, it propagates through exchanges, trading desks, and wallets without Tether needing to intermediate each transaction.

In many parts of the crypto ecosystem USDT functions as the default quote currency. On exchanges where direct banking access is limited or inefficient, USDT substitutes for dollars. Traders use it to move between positions, post collateral, and settle trades. Liquidity in many pairs is deeper in USDT terms than in fiat terms. Stablecoins have essentially transformed how dollar distribution can be approached. Unlike a bank that operates within a single jurisdiction, Tether issues USDT across multiple blockchains that are geographically agnostic.

Its massive cash flow engine has resulted in an investment portfolio separate from the USDT reserves valued at over $20 billion. A useful way to think about Tether’s strategy is that it is recycling cash flows from its highly profitable stablecoin businss into platforms and assets that could make that network harder to displace.

Some of this is directly tied to USDT distribution and settlement. Some of it is adjacent, like tokenization, wallets, Bitcoin infrastructure, and compliance. Some of it goes well beyond stablecoins into alt assets like agriculture, energy, gold, media, AI, and sports.

Despite its scale, Tether remains a private company with limited financial disclosure. It publishes periodic attestations that provide a snapshot of reserves, including allocations to Treasuries, repos, and other instruments. These attestations confirm that assets exceed liabilities at a point in time, but they are not full audits. They do not provide a detailed income statement, a comprehensive view of counterparties, or a breakdown of duration risk across the portfolio.

Tether occupies a gray area in the financial system. It performs functions similar to a bank or a money market fund, but it does not operate under the same regulatory framework. It issues liabilities that are widely treated as dollars, invests the proceeds in interest-bearing assets, and manages liquidity to meet redemptions. A large wave of redemptions would require Tether to liquidate assets quickly, and the resilience of that process depends on the liquidity and quality of its reserves.

Financials at a glance

With the base secured by Treasuries, Bitcoin, and gold, Tether deploys its surplus billions into high risk/reward tech.

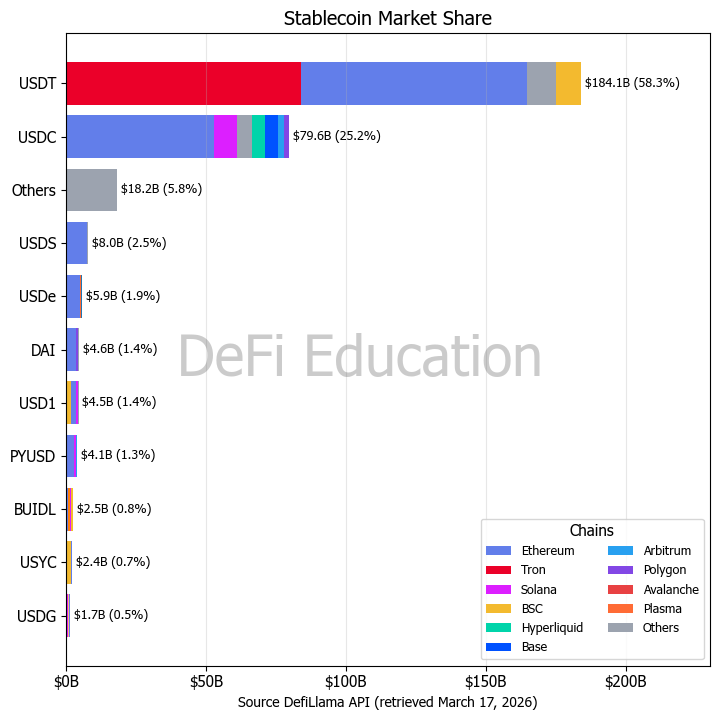

The circulating supply of USDT sits at a whopping $186 billion, making Tether the undisputed heavyweight champion of the stablecoin sector. In 2025, Tether added nearly $50 billion to its market capitalization and vastly outpaced its closest rival USDC. Tether captures ~58% of stablecoin market share.

According to Tether’s latest attestation, it held $122 billion of U.S. Treasury bills as of December 31, 2025, alongside $25 billion of reverse repos and a small amount of cash deposits. Total direct and indirect Treasury exposure exceeded $141 billion. Tether’s treasury operations have made the company one of the largest buyers and holders of U.S. sovereign debt in the world, ranking higher than the holdings of entire industrialized nations such as South Korea, Germany, and Saudi Arabia.

Tether has accumulated 96,000 Bitcoin making it one of the largest public corporate holders in the world. Unlike Microstrategy’s aggressive accumulation strategy fueled by debt, Tether’s BTC holdings are entirely unlevered, financed by its huge profits. Tether also holds ~140 metric tons of physical gold stored securely in Switzerland. The company has a target allocation of 10% to 15% in physical gold and around 10% in Bitcoin its portfolio. Its gold today would be valued at over $23 billion its BTC at ~$7.4 billion. The company also holds ~$6 billion in excess reserves which are profits retained specifically to overcollateralize USDT.

In the latest attestation on Dec 31, 2025 Tether reported:

$122.3B U.S. Treasuries

$24.8B reverse repos

$17.0B secured loans

$8.4B Bitcoin

$17.4B precious metals

$6.3B excess reserves

Controversies surrounding Tether

Anyone remember” “Tether FUD”? For years, Tether was viewed as a sketchy offshore bank. This was exacerbated by its reluctance in the past to prove its tokens were backed 1:1 by traditional fiat. Then in 2021 the New York Attorney General and the CFTC levied fines against Tether after revealing that for stretches of time between 2016 and 2018, USDT was not fully backed by U.S. dollars. While Tether has since dramatically improved its reserve quality (moving heavily into highly liquid U.S. Treasury bills) it still relies on quarterly “attestations” from accounting firm BDO. An attestation is merely a snapshot of a single day. Detractors continue to demand a comprehensive, forensic financial audit by a “Big Four” accounting firm to put the backing debate to rest permanently.

A glaring point of friction on Tether’s balance sheet is its massive portfolio of “secured loans.” During the crypto market contagion of late 2022, Tether publicly pledged to completely eliminate these loans to reduce systemic risk. Instead the value of these secured loans has ballooned to over $17 billion. Tether does not disclose the identities of the borrowers, the terms of the loans, or the exact nature of the collateral securing them. It’s fair to argue that issuing billions of newly minted USDT to undisclosed entities (especially if those entities are affiliated crypto exchanges or market makers) introduces severe counterparty risk that contradicts the premise of a safe stablecoin.

Because USDT is borderless, highly liquid, and settles instantly, it has unfortunately become a preferred medium for sanctions evasion, money laundering, and international “pig butchering” scams. To combat this and placate U.S. lawmakers Tether has increasingly weaponized its centralized “kill switch.” Over the last few years, the company has actively cooperated with the DOJ, FBI, and Secret Service to freeze billions of dollars in USDT linked to criminal wallets and sanctioned entities. This brings us to the deep philosphical paradox surrounding Tether. USDT operates on decentralized blockchains, yet Tether retains the centralized, unilateral power to freeze any user’s funds at a moment’s notice.

Risks

The first and most obvious risk for stablecoin providers like Tether is reserve composition. High quality, short duration assets reduce the risk of losses and improve liquidity in stressed conditions.

The second is regulatory pressure. Governments have become more focused on stablecoins due to their fast growing importance in payments and financial markets. Future regulation could impose requirements similar to those applied to banks or money market funds, which would change how Tether is able to operate and perhaps impact profitability longer term.

With the passage of legislation like the GENIUS Act in the U.S. (establishing a federal regulatory framework for stablecoins) and the MiCA framework in the European Union, stablecoin issuers are increasingly forced to comply with strict reporting standards, routine audits, and explicit mandates on what types of assets can legally comprise their reserves. Tether’s decided to withdraw from the EU market rather than relocate 60% of its total reserves to European banks as required by MiCA.

The third is confidence. Like any system built on redemptions, Tether depends on market trust (and the market depends on Tether’s redeemability). The system remains stable as long as users believe they can redeem at par. During the crypto market crashes of 2022 (specifically the collapse algostable TerraUSD), panic caused USDT to briefly depeg on secondary markets and drop to 95 cents. However, Tether honored billions of dollars in redemptions at parity which stress tested and ultimately validated their model to many market participants.

Tether’s Moat

Competition continues to intensify as stablecoins become more central to the crypto economy. USDC, issued by Circle, has positioned itself as a more regulated and transparent alternative, with closer ties to U.S. financial institutions. Traditional financial institutions are also exploring their own stablecoin products. Despite this, Tether has maintained its lead, largely because of its entrenched distribution and deep integration into trading.

That distribution advantage is difficult to replicate. Exchanges, market makers, and users already operate with USDT as a base currency. Liquidity attracts liquidity, and once a stablecoin becomes dominant in trading pairs, it tends to reinforce its own position. This network effect is one of Tether’s strongest defenses. Even if competitors offer more transparency or regulatory clarity, they must still overcome the inertia of existing market participants.

There is also a regulatory positioning moat, though it may end up being less defensible. Tether operates largely outside the U.S. regulatory perimeter, which allows it to move faster and serve markets that regulated issuers cannot easily reach. This is another source of controversy but it is also a source of advantage. More tightly regulated competitors face constraints on reserve composition, geographic reach, and counterparties. That limits where and how they can distribute their product. Tether’s been able to capture a ton of demand in jurisdictions where dollar access is constrained. At the same time, this advantage carries risk. Future regulation could narrow that gap or force changes to the model. However, Tether is likely in too big to fail territory and too difficult/powerful to shut down.

On Thursday’s deep dive for paid subscribers we’ll be taking a look at Tether’s investment portfolio and providing a strategic analysis.

Paid subscribers also get access to:

All of our past posts

Weekly Deep Dive Report

A comprehensive bi-weekly DeFi Roundup

Bi-weekly Q&A sessions with our team

Until next time..

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are opinions from an anonymous group of cartoon animals with Wall Street and Software backgrounds.

We now have a full course on crypto that will get you up to speed (Click Here)

We offer the Prediction Markets module on a standalone basis (Click Here)

Security: Our official views on how to store Crypto correctly (Click Here)

Do you think that the USAT they recently announced to be the 'Genius compliant' stable coin has a chance to be relevant in the U.S. and challenge Circle/USDC?