How Banks (Zeros) Make Money

Level 3 - Virgin DeFi Analyst

Welcome Avatar!

At their core, zero banks accept deposits and make loans. They are regulated institutions meaning they are monitored and supervised by government agencies.

Initially formed as a place for people to store their money with (perceived?) safety, banks have expanded to a wide range of business lines, amassing over $20 trillion in assets.

In today’s post, we’ll help you understand how banks make money and how crypto flips the entire banking business model on its head.

The world’s largest bank by assets is the Industrial and Commercial Bank of China (ICBC). That’s right - it’s not an American bank! In fact, the four largest banks are all Chinese banks. The fifth largest bank is JP Morgan, and the only other American bank in the top 10 is Bank of America.

For ease of understanding due to accounting / reporting standards, we’ll cover JPM.

Top-line: Revenues

Asset Management

The largest line item here is asset management fees - $21 billion United States Trash Tokens in 2021. These fees are earned by JPM on assets they manage on behalf of other investors. Fees are based on JPM’s $3.1 trillion Assets Under Management (“AUM”). JPM earns:

Management fees on AUM

Performance fees on returns generated on AUM (not on all funds)

Fees on related services e.g. brokerage, custody, etc.

$14 billion, or 2/3, of fees in this segment come from investing managed funds. The other major segment is brokerage commissions which are fees earned from facilitating buying and selling of securities on behalf of their clients.

Enzyme Finance: Decentralizing Asset Management

Enzyme, among others, is one of the protocols decentralizing this aspect of the banking industry.

Enzyme is an on-chain asset management protocol. Their vaults allow funds to be delegated to someone who can manage trades but not run off with your funds. Enzyme enables people to launch their own crypto funds with almost zero overhead and upfront cost. Traditional hedge funds can easily cost 6-7 figures to launch and maintain which can make launching low AUM hedge funds difficult.

If you take into account lackluster returns across many funds, it’s clear that JPM’s largest line of business is under threat by decentralized alternatives.

Anyone can become a fund manager. In the future of finance, you don’t need to go to Wharton and have millions of dollars to raise a fund.

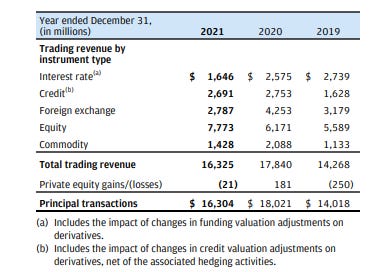

Principal Transactions

JPM’s Principal Transactions business is primarily comprised of market making / trading and risk management (derivatives).

$16 billion United States Trash Tokens earned by this activity in 2021.

Since the Volcker Rule was introduced in the wake of the 2008 financial crisis, banks’ proprietary trading activities reduced so the revenue you see above relates to servicing client business - market making - rather than the bank using its capital to speculate. JPM’s customers need to buy / sell stocks, foreign exchange, and other financial assets: the bank “makes a market” to allow them to trade and charges a fee by selling to clients at a higher price than it is willing to buy from them.

Where else have you seen the term market making before? In our various posts on DEXs and liquidity providing in crypto! Crypto has already decentralized market making by way of liquidity providing. JPM is acting like a permissioned Uniswap pool for every asset which it trades with its customers.

Crypto certainly has a long way to go before market making of traditional assets can be done on-chain at scale (barred primarily by regulations).

However, regulations cut both ways: for example retail investors in Europe are prohibited from investing in US ETFs like SPY (tracks S&P 500) and QQQ (tracks Nasdaq). The time will soon come when Europeans (and underbanked people) can access a US stock index tracker on a DeFi protocol like Synthetix, permissionlessly, without being affected by regulations.

The future for market making in the medium term likely looks like some combination of sources. Some market making loses out to on-chain, some will remain with crypto native institutions, and perhaps some will remain with banks who adapt to crypto appropriately.

One thing’s for sure - this aspect of JPM’s business will come under pressure down the road.

Investment Banking

If you’ve been reading DeFi Education, you should know what this is by now! Investment banking was covered in-depth by Owl in his personal update.

That said, let’s dive into briefly from a business perspective.

Investment banking can be broadly bucketed in two segments:

Advisory (e.g. M&A, restructuring)

Raising capital (e.g. IPOs, underwriting / syndicating loans and bonds, etc.)

Investment bankers are transaction-oriented, meaning they get paid primarily for originating, managing and closing transactions across advisory and capital raising engagements. They get hired by companies to market the company to a broad base of institutional and strategic investors and lead them to a successful outcome.

Banks reap massive fees for these services. In the case of JPM, their revenues are relatively evenly split across equity / debt / advisory. JPM is a bank with a “balance sheet” which means they can use their huge balance sheet to finance deals. This gives them a more holistic set of capital markets services for companies and helps them win advisory deals.

Bowtiedbull made a great case for why Equity Capital Markets is going to zero.

The TLDR is that all bankers are doing in capital raising transactions is finding investors to buy coins. In the world of the internet and cryptocurrencies, you can largely cut out the middle man (who charges 5-7% of the raise) and go direct to your investors.

Advisory, however, is unlikely to be disrupted by crypto. There is still value in relationships, trust and expertise. Hence, the bank’s M&A business can adapt to change simply by bringing in and hiring the right people (although we are quite bearish on their ability to do that in the long run and believe the brain drain from TradFi will continue).

Lending and Deposit (Fees Only)

The next big segment of non-interest revenue is lending and deposit fees. Note that this is separate from the fees earned on the spread earned between bank deposits and loans.

Of the $7 billion United States Trash Tokens earned in 2021, $5.6 billion came from “deposit-related fees.”

Hmm.. Wonder what that is.. 🤔

These $5.6 billion in deposit-related fees are largely earned from overdraft fees. These are fees charged to people who run out of money in their account and swipe their card, often charged $25-$35+ a transaction for so-called “processing” (wonder what the margins are on this processing).

According to the Consumer Financial Protection Bureau (CFPB), 9% of customers pay 10 overdraft fees a year and account for 80% of all overdraft revenue. These are huge revenues for banks - talk about a misalignment of incentives.

In crypto you manage your own deposits. Your fees are gas which, on Ethereum today, are even worse than bank overdrafts. However, if you can avoid Ethereum mainnet and responsible with self custody, crypto is a far superior option to hold your savings than a bank.

Card Income

Card income refers to income from credit and debit cards and interchange fees.

Autist note: Interchange fees are the component of card payment fees paid to the cardholder’s (i.e. your) bank. They represent the largest component of fees and can be upwards of 2% in the U.S. (0.3-0.4% in EU).

Crypto represents a new way of payment entirely that bypasses rent-seeking banks. As your own bank, you can pay directly to merchants and cut this process out. Yes, there will likely be a payment processor in between in these early years of blockchain technology, but in the long run direct Consumer <> Merchant transactions should be seemless.

Card Income = Zero.

Other Income

Other significant sources of non-interest income for JPM are operating leases (~$4.8 billion) and mortgage lending and related services ($2.2 billion).

As covered in our posts on Real World Assets here and here, these areas are likely far in the future disruptions. It’s not that the solutions being built don’t work, it’s that scaling and trust are two major challenges we see today that do not have an easy solution.

However, we are optimistic so we will throw out a wild guess and say this will be resolved by the back half of this decade as there are tons of people trying to figure this out and RWA represents a deca-trillion dollar opportunity.

Net Interest Income

Total Non-Interest revenue represents roughly $69 billion, or 57%, of JPM’s total ~$122 billion in revenue. The remaining $52 billion is Net Interest Income, the revenue item you might know banks for best.

Net Interest Income (NII) is the difference between the interest it earns on lending activity and interest it pays on bank deposits.

As of December 31, 2021, JPM held $1.8 trillion in deposits it paid interest on.

How much did JPM pay out in interest bearing deposits? $531 million, or 0.03%. Even if we look at total interest expense as a function of total deposits, they only paid out 0.3%.

If you’re a bit confused here, think of “Net Interest Income” in terms of Gross Profit (earnings before operating expenses, taxes, etc.). JPM’s gross profit on interest-bearing assets and liabilities is 89%.

In a world of self-custody and cryptocurrencies, you can start to see how at least some portion of these deposits will move away from banks.

Concluding Thoughts

You’d be hard pressed to convince us that 100% of the world is going to be able to self custody their assets with the state of the user experience as it is today. But. Crypto is very clearly eating away at the various parts of banks’ revenue streams.

Slowly, then all at once.

This is a free article. We are a niche research publication building an in-depth fundamental analysis and educational platform to give crypto users and investors better odds against VC Funds, influencers and whales that control the market. We teach you to think like them.

Our publication relies purely on content quality and word of mouth to grow so we would appreciate if you could give this article a share.

In our paid substack, we dive deep into protocols and tokenomics as well as provide broader market commentary. Thousands of readers trust us for our analysis. No frills no shills.

Join our community below.

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are opinions from an anonymous group of cartoon animals with Wall Street and Software backgrounds.

Great post!

Late to the game here, but would be more interested in your thoughts on Chinese banks. I didn't realize they were the top 4! Why is this? Are they managing gov funds or customer's funds?