Making Bonds in DeFi

Level 3 - Virgin DeFi Analyst

Welcome Avatar!

A common criticism of DeFi is that it operates in a “closed-loop.”

Applications serve tokens for other applications that serve tokens for other applications, with no linkage to the “real world.”

You’ve heard us say the words “DeFi relies on speculative activity” numerous times.

Regardless of how you frame it, it is now a commonly held belief that there is no foundation for DeFi that is based in the real world.

“Real world assets” is a segment within crypto that aims to use blockchains to connect to off-chain assets, combining “real” assets with DeFi, NFTs, etc

We delineate between tangible off-chain assets and intangible assets (referring largely to in-game assets). Tangible off-chain assets are anything where the ownership is not digital, such as homes, cars, apples, and even websites (even though websites are digital, the ownership is contractual).

Why are we delineating between tangible and intangible assets? The regulatory implications are different.

For RWAs to become widespread there will have to be interaction with the local legal and regulatory systems. Crypto native assets can exist outside the control of governments, but from a practical perspective RWAs will need the backing of laws. Scaling RWAs will require commercial activity, which means assets will need standard contractual protections and legal assurances that allow businesses to transact in the real world.

We make an exception for gaming because video games are their own closed systems where the game’s creators determine the laws of the land. However, blockchain gaming will probably still need to overcome securities laws as they pertain to token issuance and trading.

RWAs require give and take on both sides. Regulators and corporations have to push for accommodative policies. Crypto participants have to work on projects that capture assets in the real world.

Some DeFi founders are doing exactly that.

SuperState Short-Term Government Bond Fund

Last week, the founder of DeFi project Compound announced SuperState. Co-founder Robert Leshner left Compound, and the new CEO of Compound was an internal promotion.

The fund has preliminarily registered with the SEC and plans to invest 95%+ of its net assets in short-duration U.S. government securities, including treasury, government agency securities, and repurchase agreements.

In other words, it’s meant to be a boring, stable income fund. The management fees are 0.33%.

The shares will be quoted on Ethereum, but the “source of truth” will be a transfer agent. Use of the shares on Ethereum is entirely optional.

Autist Note: A transfer agent is a trusted third party appointed by a corporation or mutual fund to track and manage the record of ownership of its securities. Basically a back office function handled by banks or trust companies.

SuperState is aiming to bring a low risk, low yielding investment fund product to crypto for users who are willing and able to KYC to access off-chain yield and get government bond exposure. This is a permissioned product.

The blockchain aspect is more like a cherry on top, for now.

What’s the Angle?

We were racking our brains for a while to answer this question: why do this?

It’s permissioned, which likely eliminates a swath of crypto whales with long-term capital on-chain.

Accessing the fund on-chain is optional, eliminating most if not all tradfi institutions.

Is this just another attempt at RWA that will remain niche and never scale?

The remaining participants are:

Crypto native funds

DeFi protocols

Crypto retail

1 & 2 are the most interesting to us, where as 3 is more like optionality (crypto retail is notoriously fickle when it comes to adopting and staying with new products).

Crypto Native Funds

Funds are going to be less apprehensive about KYC and still want to keep their capital on-chain to make trades opportunistically. Access to U.S. treasury yields would be an attractive way for funds to diversify, especially in between the long drawn out bear market cycles with slower activity that crypto is accustomed to.

DeFi Protocols

DeFi Protocols can have multiple reasons to use this product. The first would be deploying their treasuries to capture “risk free” yields.

In the current stablecoin model, the issuer earns (and keeps!) the interest earned from investing the dollars backing stablecoins in short term government securities. During the bull market, interest rates were low and depositing stablecoins on a DeFi lending platform generated returns well above the risk free rate.

When short term rates are nearly 5%, as now, it becomes a significant headwind to deploy cash in stablecoins with low or no yield. This product solves that problem. But. The filings don’t disclose any evidence that the yield will be paid out on chain. At best, buying shares in this trust on chain means that interest will be paid out to your real world, KYC-linked account.

However, this may make sense for larger DeFi organizations like MakerDAO, whose co-founder Rune Christensen responded to Mr Leshner’s Twitter announcement of the product by requesting a feature to solve for a bankruptcy risk concern. It seems that large holders of or issuers of stablecoins are potential customers for this model.

Autist note: Rune’s primary concern is the potential liabilities of the issuer in relation to the tokenized asset. If the company gets sued or loses a lot of money, token holders could face problems. If the company goes bankrupt, the people the company owes money to might try to claim the assets linked to the token. If that happens, token holders might only get what's left after all the debts are paid. While it's unlikely that these creditors could take the token holders' money, they might be able to freeze it. This could stop token holders from withdrawing or redeeming their money for a long time while legal issues are sorted out.

Finally, as the founder of Compound, Robert Leshner will have a lot of relationships in the DeFi ecosystem. This could help him source crypto capital to this fund and other funds launched by SuperState. And. There’s a possibility that on-chain shares in these trusts could become accepted collateral for borrowing on DeFi platforms like Compound. COMP tokens are up 100% since June 24, but there is no explicit connection between Compound the protocol and SuperState (beyond the founder of course).

Could this be a long-term competitor to USDC? The permissioned nature is a drawback, but regulators may disapprove of instantly tradable bearer instruments like USDC and eventually mandate KYC and whitelisting for US-headquartered stablecoin issuers.

A more cynical view is that this is essentially a nothingburger for the blockchain space. As it stands, it’s a traditional mutual fund structure that does not have critical blockchain features. Any future feature it does have will be optional in nature. And while we believe there is a lot of potential for on-chain funds, this falls short of our expectations for what is considered “on-chain.”

Here’s are the advantages a truly tokenized mutual fund could offer:

Automation: Automating processes in the mutual fund industry, such as the buying and selling of fund shares, which can speed up transactions and reduce costs.

Transparency: Investors can independently verify transactions and holdings.

Global Market Access: On-chain funds can be accessed by investors around the world, opening up new markets for fund managers.

Real-Time Trading: Unlike traditional mutual funds, which are typically priced and traded at the end of each business day, on-chain funds could be traded in real time.

Should COMP be up 100%? Not off this news - at least not until we have far more information about any explicit connection. In addition, apparently SuperState won’t even whitelist protocols! This essentially breaks interoperability. However, it’s possible this is a play for Minimum Viable Regulatory Approval (we just coined this term). SuperState may add more funds to its portfolio which may interact with protocols.

A key consideration here is that funds of this sort have been approved already. Franklin Templeton’s OnChain U.S. Government Money Fund has $292 million in assets currently, and is available on both Ethereum and Polygon.

There are already competitors! So what’s the deal? Maybe this is just a way to collect some cash flow for the founder. 0.33% with $300 million in assets would net $1 million a year. It doesn’t seem to us that this would be a needle mover for the founder of something as successful as Compound, but we’re not here for pocket watching! A more optimistic view would be that SuperState wants to become the leading blockchain investment firm. The Franklin Templeton for crypto.

Regardless, it’s not logical to us that COMP tokens should respond so strongly to this news. While we did get the itch at first, we’re not shorting COMP (or anything else) for the reasons below.

AAVE is up ~50%, and DeFi in general has performed well (meanwhile NFTs have gotten crushed!). The market could catch another bid.

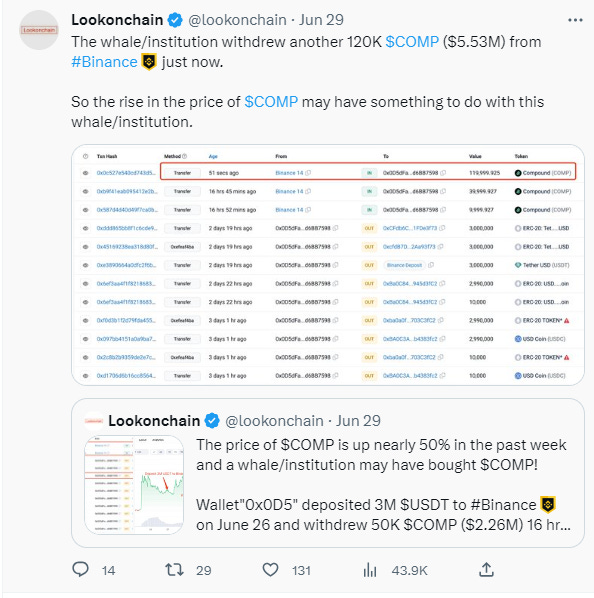

Finally, there are signs that indicate large buys of COMP token which when combined with the run up on the tokens leading up to the announcement could mean there is information we are not privy to. In essence, this is not high conviction enough for us like some of our past ones for paid subs! Caveat emptor.

This is a free post. Consider becoming a paid member for more expert insights.

Until next time..

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are opinions from an anonymous group of cartoon animals with Wall Street and Software backgrounds.

We now have a full course on crypto that will get you up to speed (Click Here)

Security: Our official views on how to store Crypto correctly (Click Here)

I think VitaDAO just fractionalized IP on chain using one of their IP NFTs. They're working with a company in Switzerland for legal stuff, but they might be leading the onboarding of RWAs.