New Stablecoin Cabal?

Level 2 - Value Investor

Welcome Avatar!

CRCL’s stock is down 16% today as a group of over 140 companies just announced they’re launching a stablecoin together. These companies include Visa, Mastercard, Stripe, BlackRock, Coinbase, and Google. Notable absences from the list include Circle, Tether and PayPal.

As usual, peak emotions and major market moving news are triggers to make a closer analysis and decide whether to buy / sell an investment.

Background on Open Standard

Open Standard is a new company led by the co-founder of Bridge (acquired by Stripe for $1.1 billion in early 2025). Today they unveiled Open USD (OUSD), a stablecoin to be launched later this year on Tempo, Solana, Base and more.

The pitch is that Open USD isn’t a typical issuer-led stablecoin where one company controls the coin, the reserve relationship and all the interest income.

As mentioned in our recent CRCL coverage, stablecoin issuers like Circle make money by taking the dollars backing the USDC in circulation and earning yield on them by buying short-term treasuries. We suggest reviewing our coverage to understand how we think about Circle’s business model.

Open USD will allow businesses to mint and redeem OUSD with no fees or volume caps. Businesses can mint and redeem at no cost and OUSD’s partners receive reserve earnings. Open Standard will earn a small management fee on reserve earnings. Governance is also supposed to sit with Open Standard as an independent company with a board made up of Open USD partners rather than being controlled by a single issuer.

The partners list includes payment companies, fintechs, exchanges, banks and commerce platforms. All these companies have an incentive to use stablecoins. As profit motivated entities they also have an incentive to keep more of the reserve income for themselves.

The market is pricing in two main risks from this news:

The partner list means Circle’s distribution channels have competing interests, with even Coinbase joining the group (USDC’s most important distribution partner)

Most of the yield from OUSD goes to the partners which can rework the distribution model for stablecoins and pressure Circle’s margins if they have to compete

OUSD Likely Overblown Based on Facts Today

Open USD is not live yet. It has no public redemption history, no proven liquidity and no operating record. There is no likely no material 2026 P&L impact. Launch details and broader mechanics are incomplete.

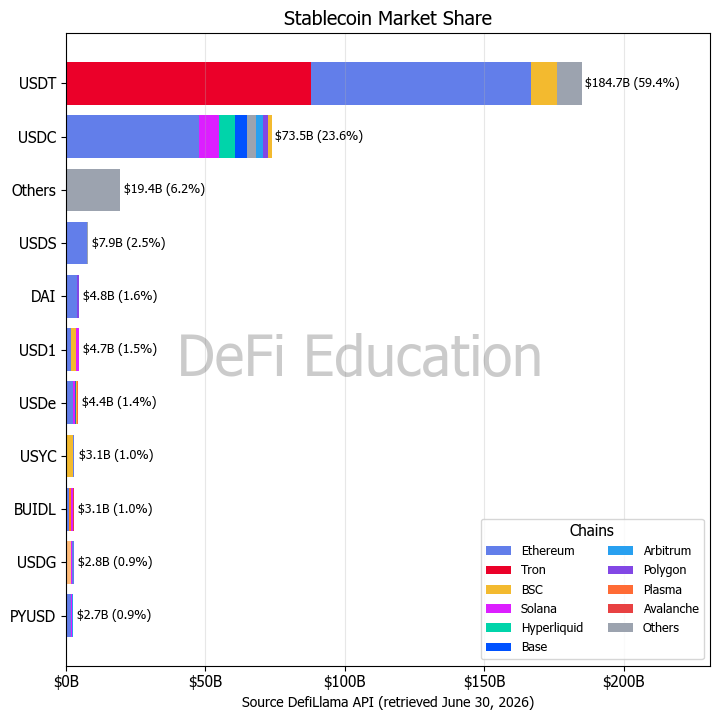

USDC, by contrast, is already deeply liquid, widely integrated and trusted by institutions. It has years of redemption history, major exchange support, DeFi integration and regulatory positioning.

We have also been part of the crypto industry for long enough to know that simply slapping a bunch of corporate logos onto a launch announcement doesn’t mean the product will live up to expectations.

OUSD is not really an innovation in terms of the core model level. White label stablecoins already exist (Paxos’ “stablecoin as a service” model). PayPal’s PYUSD is another version where PayPal owns the customer facing distribution and Paxos handles the issuance and custody.

In 2024, Paxos launched USDG (Global Dollar Network) with a list of partners that included Robinhood, Kraken, Anchorage and Bullish. Partners Could receive up to 100% of returns generated by assets backing USDG held on their platform and earn additional revenue for minting and acceptance activity. Since its launch in November 2024 it has grown to ~$3 billion in circulating supply. Despite this headline number (which is still significantly smaller than USDC) there are only about 5,000 USDG holders on Ethereum. It never gained real consumer traction.

OUSD is not a new collateral model, not a new peg mechanism, and not a new form of yield generation. It is still the same basic business where you issue a dollar token, hold cash/T-bills, earn reserve income, then decide how you split up the economics.

If you must point out an innovation here it’s simply who they were able to get into the room as part of their launch. Many of the partners in this case are payments and commerce heavy. Visa and Mastercard are the dominant global card networks, Stripe is the payment processor for a large share of internet commerce, and Google and Shopify control distribution into hundreds of millions of end consumers. The list also includes Coinbase which is a key distribution partner for Circle.

Innovating on distribution can be a competitive advantage when launching a new product, but in our view it’s a stretch to ascribe full value to this single competitive threat. The real question is OUSD’s adoption which anyone who’s been in crypto for more than one cycle knows is extremely difficult to obtain.

Extension of Stripe’s Worldview

In 2025, Stripe announced “Open Issuance” powered by Bridge arguing that businesses building on externally issued stablecoins cannot fully capture the benefits of the underlying reserves. Open Issuance let businesses launch and manage their own stablecoins. If we were to speculate on what happened, it’s unlikely businesses were interested in launching their own stablecoins. OUSD is an attempt to give businesses the benefit of shared economics without having to deal with the management of the stables.

Circle x Coinbase

We’ve seen some surprised faces around Coinbase’s participation and active promotion of OUSD. There doesn’t seem to be anything that prevents Coinbase from participating in another stablecoin consortium, just like there isn’t anything preventing CRCL from entering distribution deals with other third parties.

Coinbase and Circle have a Collaboration Agreement they entered on August 18, 2023. This automatically renews for another 3 years as long as threshold criteria are met, even if the parties do not agree on modifications.

In other words, before the initial term lapses Circle and Coinbase discuss in good faith whether changes are warranted. If they do not agree on changes, the agreement automatically renews for additional three-year terms unless either party fails to meet ongoing obligations under the agreement.

Coinbase gains some amount of leverage to negotiate economics in the future if OUSD actually gets traction. We’d consider any negotiating leverage today to be a bluff because Coinbase likely cannot simply demand worse terms and force Circle to accept them. If Circle refuses new terms and both parties have met the threshold criteria, the existing agreement should renew anyway (some contract details are redacted).

The Circle and Coinbase partnership is quite interesting because each represents meaningful business to the other party, but also a meaningful cost. They are incentivized to see USDC grow, but also to diversify exposure from the other to ensure a single partner does not threaten a core business line.

CRCL Stonk

The stock market is generally bad at pricing this type of risk because there are two different things happening at once. And. Sometimes portfolio managers in large caps want to clear the risk from their books first, then do research and decide what to do.

From a finance perspective there’s little immediate impact because OUSD doesn’t exist today. CRCL’s next few quarters are going to be driven the same drivers we covered in our latest post.

From a narrative perspective this can hurt Circle because it points out that the companies best positioned to embed stablecoins into actual commerce may not want to route that growth through Circle if there’s a more lucrative model for them. Since these companies serve as the gatekeepers they can work with both Circle and Open Standard in parallel and simply side with the eventual winner.

On an adjusted EBITDA basis CRCL traded at a 29x EV/LTM Adj. EBITDA prior to the OUSD announcement and now trades at 24x LTM Adj. EBITDA. CRCL doesn’t trade at depressed valuations. CRCL still prices in strong growth, USDC maintaining its moat and an ability to preserve attractive economics over time.

Concluding Thoughts

Our take is that OUSD’s key potential innovation is its partners list. Most companies likely signed up because it is cheap strategic optionality for them, while only a smaller subset would use OUSD meaningfully if it works. It’s a bet with little downside and good upside for the partners. With Stripe being a key partner and Open Standard being spearheaded by the co-founder of Bridge, this bet was easier to make reputationally. However, it still remains a bet.

While we do think the announcement is worth taking seriously and we intend to monitor the launch of OUSD, we don’t think it’s worth blindly extrapolating a broad shift to the stablecoin business model today. We will provide another Circle update after its launch (likely for paid subs only) if there is market moving information.

Paid subscribers also get access to:

All of our past posts

Weekly Deep Dive Report

A comprehensive bi-weekly DeFi Roundup

Bi-weekly Q&A sessions with our team

Until next time..

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are opinions from an anonymous group of cartoon animals with Wall Street and Software backgrounds.

We now have a full course on crypto that will get you up to speed (Click Here)

We offer the Prediction Markets module on a standalone basis (Click Here)

Security: Our official views on how to store Crypto correctly (Click Here)