Stablecoins: Reinventing Dollars

Level 1 - NGMI

Welcome Avatar! Today, we dive into a beginner’s guide for stablecoins. Stablecoins are cryptoassets backed 1:1 by another asset (most commonly USD). They can be backed by equivalent assets, collateral or math.

We’ll dive into the various categories of stablecoins and go over a few examples.

Stablecoins have become one of the largest asset classes in crypto, not only capturing significant market cap but also creating value for applications built around them such as MakerDAO, Curve, Abracadabra, etc.

Primary use cases for stablecoins:

Trading in and out of other cryptoassets without going off-chain (e.g. no need to cash out via an exchange)

Store of value (global access to USD)

Leveraged long positions using collateral

Remittance and money transfers

Yield farming

The most commonly known stablecoins are USD Tether (“USDT”), USD Coin (“USDC”) and DAI. Other major coins include Binance USD (“BUSD”), Terra USD (“UST”), Magic Internet Money (“MIM”) and FRAX.

Centralized Finance (“CeFi”) Stablecoins

USDT and USDC are the largest centralized, custodial stablecoins with $77 billion and $41 billion in market cap, respectively. Founded in 2014, USDT was one of the first stablecoins in existence. USDC was not founded until years later in 2018.

Across the board, stablecoins have seen a parabolic rise in the last two years, with not just USDT and USDC, but various decentralized solutions achieving wide adoption.

With a direct link to other cryptoassets, 24/7 availability and immediate international transferability, it’s no surprise that stablecoins continue to grow in popularity. Stablecoins provide international access to USD liquidity.

In fact, stablecoins also represent a growing share of transactions compared to non-stablecoins such as ETH and BTC as a medium of exchange. USD stablecoins have roughly 10x the daily dollar transfer value of ETH, and 4x BTC.

While USDT is only 1.9x bigger than USDC in terms of market cap, 24h volume for USDT is $59 billion compared to $4.4 billion for USDC.

USDT is by far the most liquid stablecoin for trading.

CeFi stablecoins are intended to be backed 1:1 by fiat currency held in deposit. 1 USDT should be directly backed by 1 USD in their reserve.

Here’s how a CeFi stable like USDT maintains its peg:

Price of 1 USDT in the market falls from $1 to $0.99

Iguana buys 100 USDT in the open market for $99 and converts the USDT to $100 via Tether

Iguana pockets $1 in profit

When Iguana deposits the USDT to Tether, the USDT is burned

In the reverse scenario (1 USDT = $1.01), Iguana could deposit $100 with Tether to mint 100 USDT, then sell then USDT in the open market for $101 pocketing $1 in profit

This arbitrage activity helps maintain USDT peg close to $1

In a perfect world, if everyone knows USDT is backed by $1 and that $1 being there is entirely riskless, USDT should always be worth $1.

USDT is run by Tether Limited (an entity of Hong Kong exchange Bitfinex), USDC is run by Circle, and BUSD is issued by Paxos in partnership with Binance. Centralized stablecoins are subject to significant regulatory and counterparty risk. However, at the moment, they are critical infrastructure in crypto markets and serve as the backbone of trades, with USDC being the most common trading pair in DeFi.

Stablecoin issuers Tether and Circle earn revenue from applying creation and redemption fees, but they seek further profit by lending out their reserves. As stablecoins are redeemable on demand but the dollar reserves have been loaned to companies for a fixed term (commercial paper), the issuers could not pay out $1 to each stablecoin holder immediately. They would need to sell the collateral or wait for the loans to mature. This is known as a liquidity (or duration) mismatch. In times of extreme market volatility or suspicion about an issuers’ ability to pay out in US Dollars, stablecoin holders may start to redeem their tokens, causing a ‘bank run’. This could cause losses for remaining holders and potentially systemic effects in DeFi due to the wide use of stablecoins and the assumption that they will always be worth $1. This risk has been noted at the highest levels of TradFi, appearing in the most recent quarterly review by the Bank for International Settlements.

Note: as long as DeFi is dependent on CeFi stablecoins, DeFi is dependent on traditional finance. We believe establishing a truly decentralized stablecoin is one of the most important problems to solve in crypto.

Decentralization is not binary - it’s a gradient. We’ll move on to some of the stables making a run at decentralized solutions.

Collateralized Debt Position Stablecoins

Collateralized Debt Position (“CDP”) - a fancy term to indicate borrowing against collateral (e.g. deposit ETH → Borrow stablecoin). In bank terms, think of your deposit as your equity and the borrowed asset as a liability that must be repaid to retrieve your deposited asset.

CDP stables rely on an overcollateralized pool of cryptoassets, meaning the collateral pool is worth more than the stablecoins generated against it. Overcollateralization adds financial security to the system, and users can be liquidated if the value of their cryptoassets falls below a predetermined collateralization ratio (the inverse of Loan-to-Value).

The largest CDP stables are DAI and MIM.

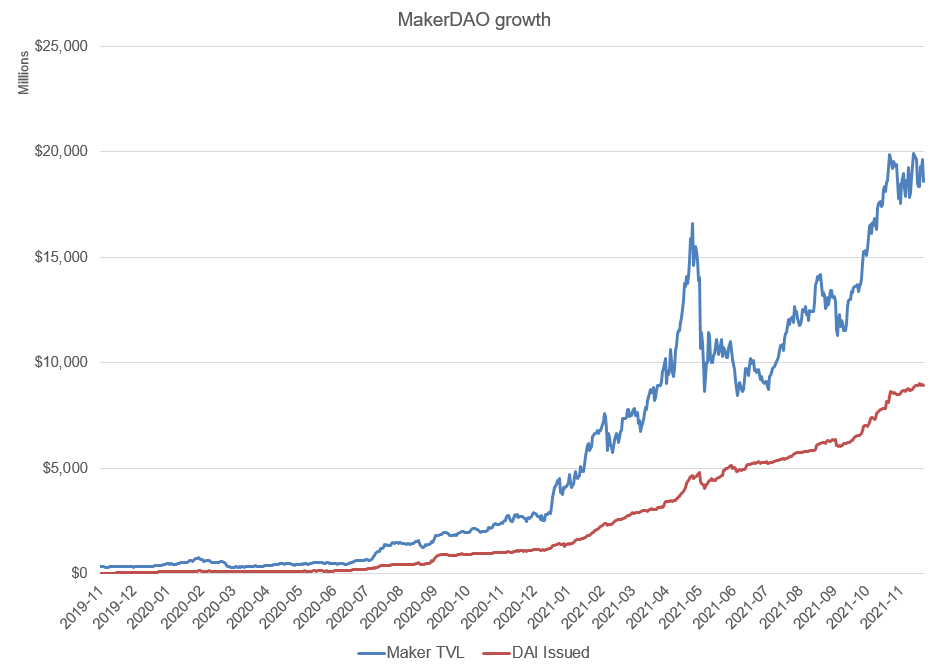

The largest, most successful and lindy decentralized stablecoin is MakerDAO’s DAI. Paid subscribers can learn more about MakerDAO here.

Despite the negative press MakerDAO has received in recent months as a result of increasingly being backed by USDC (a centralized stablecoin), losing the multichain battle to UST and MIM, and some internal conflict, DAI today remains the dominant, most battle tested decentralized stablecoin on Ethereum having survived brutal market conditions over many years.

MakerDAO has active plans to expand collateral options to include Real World Assets and has attracted institutional interest. Societe Generale recently approached MakerDAO to refinance part of a 40 million Euro bond portfolio backed by residential mortgages.

Here’s how a CDP stable like DAI maintains its peg:

Iguana borrows 100 DAI ($100) at a 1:1 ratio from the Maker vault

Price of 1 DAI in the market falls from $1 to $0.99

Maker’s Oracle still considers 1 DAI to be equal to $1

That means Iguana can now buy 100 DAI for $99 and pay back the DAI owed to the Maker vault, pocketing $1

When Iguana pays the DAI back, the DAI is burned which reduces supply

In the reverse scenario (1 DAI = $1.01), Iguana could borrow 100 DAI more from the Maker vault and sell it in the secondary market for $101, thereby pocketing $1

This arbitrage activity helps maintain DAI’s peg close to $1

If you’ve read between the lines, you probably realized that DAI is much harder to scale primarily because it needs to be overcollateralized. Stablecoins have been very expensive to borrow for most of the year, with rates often at 10% or more above the official USD interest rate (the Federal Funds Rate set by the United States Federal Reserve). Why might this be?

Centralized stablecoins can only be created when a customer deposits fiat currency with the stablecoin issuer. Collateralized stablecoins can only be created when a borrower locks up collateral. Despite limited supply, stablecoins are in very high demand due to all the use cases listed above, and we believe that the high borrow rates on stables are a result of this supply/demand imbalance.

What if a type of stablecoin could be created where it was easier and more capital efficient to expand the supply to meet user demand?

A potential solution to the poor capital efficiency and limited supply of CDP coins is algorithmic stablecoins. An algorithmic stablecoin can be issued at will, it does not need to be fully backed by collateral, and therefore can expand its supply to meet market demand easily.

UST, a hybrid CDP / algorithmic stablecoin has gained significant ground recently, developing its ecosystem on the Terra (LUNA) blockchain and expanding to other chains beyond Ethereum. We say hybrid because UST is *not collateralized*. Instead, UST is backed by an algorithm that incorporates LUNA, the reserve token for the Terra blockchain.

1 UST can always be exchanged for $1 worth of LUNA. In order to mint 1 UST, $1 worth of LUNA must be burned. Conversely, minting 1 LUNA requires burning 1 UST.

Here’s how UST maintains its peg:

Price of 1 UST falls from $1 to $0.99

Iguana buys 100 UST in the open market (e.g. off-chain CEX) for $99

Iguana uses the 100 UST to mint $100 worth of LUNA by burning 1 UST

Iguana pockets $1 in profit

In the reverse scenario (1 UST = $1.01), Iguana could buy $100 of LUNA on the open market and burn it to mint 100 USDT, then sell then USDT in the open market for $101 pocketing $1 in profit

This arbitrage activity helps maintain UST peg close to $1

The cost of volatility for LUNA is borne by validators who experience the impact of inflation of LUNA supply when UST is contracting from downward pressure. We will cover LUNA in more depth in a future post, but this should give readers an understanding of the high level mechanics behind LUNA/UST.

Algorithmic Stablecoins

Algorithmic stablecoins are stablecoins that are typically not backed in full by collateral and rely on an algorithm to maintain price. Smart contracts outline the process for minting and burning of tokens that serve to maintain the price peg of each token.

In simplified terms, the typical mechanism involves a stablecoin and a token that profits from stablecoins being issued (seigniorage shares). Rising demand for the stablecoin increases its price above $1.00, which creates new supply that brings the price back to $1.00. When price falls below peg, stablecoins are removed from circulation by burning tokens.

Importantly, algostables do not have collateral and have no proven way to prevent a downward spiral that wipes out the value of the coin. There have been many previous iterations of algostables that have royally failed.

Incentives (buying the stable below the peg will result in a profit *if* the peg is restored) do not work in times of panic because of game theory and the beliefs of market participants.

When there is a bank run type of event, investors who exchange their risky asset for safe collateral first fare best and those who are late are forced into heavy losses. Other economic incentives which are likely to fail include trying to control supply/demand for a stablecoin by setting interest rates.

In some designs, when the stablecoin breaks below the peg, interest rates are increased to discourage selling and induce buying – you can stake your stablecoin with the protocol which temporarily removes selling pressure. This is like governments attempting to prevent their currency from failing by raising interest rates at the central bank. This doesn’t work.

History shows that capital flight results: investors want to trade the risky currency for a safer asset, usually US dollars, because they believe high levels of interest will not be enough to offset the loss from currency devaluation. In DeFi, 5,000% APY isn’t good enough if you buy a stable for 90 cents and can only sell it for 2 cents one year later. This was the fate of Empty Set Dollar, an algorithmic stablecoin which broke its peg last December and never recovered.

Not all hope is lost, however.

OlympusDAO (OHM), discussed at length in past articles, is also an algorithmic stablecoin that is not bound to a peg. OHM aims to create a stablecoin that is not pegged to stable currencies, thereby achieving stability as a truly crypto-native reserve currency.

Fei is a stablecoin that uses Protocol Controlled Value to backstop risk.

Algorithmic stablecoin Frax is a fractional-reserve stablecoin that is partially backed by collateral (and will be covered in-depth in our next article). Both Frax and UST share design similarities and have successfully maintained their peg.

Closing Thoughts

We hope you enjoyed reading our introduction to stablecoins. We know the question you have arrived at: what will win?

It’s not clear today which stablecoin models will be the eventual winners - CeFi stables, CDP stables, algo stables or some future DeFi concoction.

With rising regulatory oversight, we plan to place our bets on decentralized solutions. Whether these decentralized solutions will be backed by cryptoassets, fiat, or purely mathematical solutions is to be determined.

One thing’s for sure - stablecoins are a critical component of DeFi and (in our opinion), global financial infrastructure.

Until next time, anon..

If you’re reading this and haven’t subscribed yet, join our community of DeFi Turbo Autists below!

Disclaimer: None of this is to be deemed legal or financial advice of any kind and the information is provided by a group of anonymous cartoon animals with backgrounds in Wall Street and Software.

Great article as always man!

"Iguana uses the 100 UST to mint $100 worth of LUNA by burning 1 UST"

Believe this part should be burning 100 UST instead of 1 UST. Thanks!

Nice intro article.

Balaji has articulated an interesting related concept — "flatcoins". These wouldn't be pegged to a fiat currency, which is an inflationary asset. Flatcoins instead could track real purchasing power in a "flat" manner, as measured against weighted, dynamically calculated baskets of consumer goods prices. Broader application outside DeFi but thought-provoking in any case.

There was an open call for a development grant, not sure on status — https://1729.com/inflation