Update on Valuations and The State of DeFi

Level 2 - Value Investor

Welcome Avatar!

Today we compare changes in key DeFi metrics from last summer to present.

We’ll take you through a per segment overview, discuss some key narratives, and share some research ideas we’ll be covering in more depth for paid subscribers.

Let’s dig in.

High Level Overview

DeFi last summer was simple. Core financial primitives on the blockchain. Decentralized banks, stock exchanges, and a automated hedge funds like Yearn.

Over the last twelve months we’ve had dozens of new ideas spring up.

Hype and valuations were high, but which of our core protocols stood the test of time and where are we researching now?

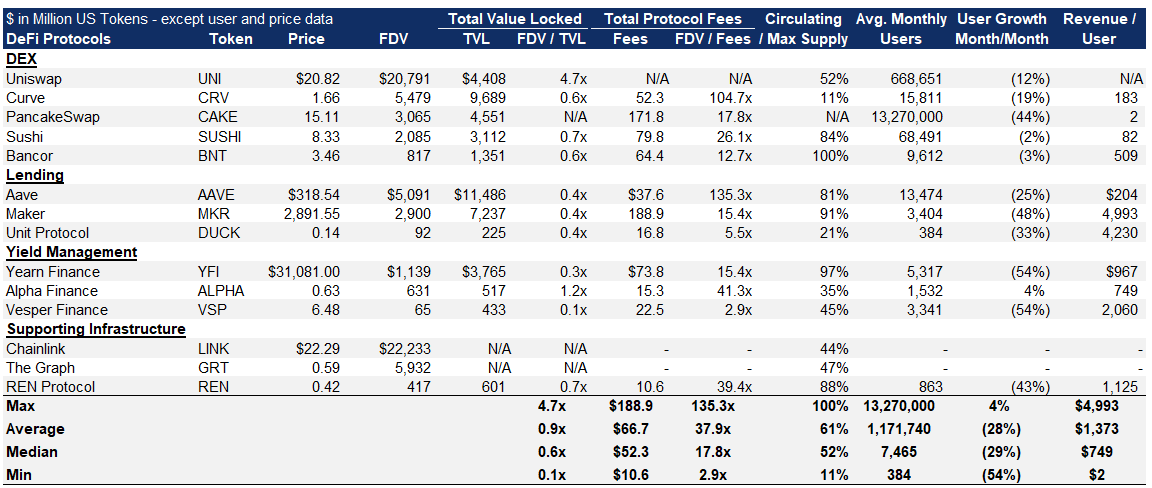

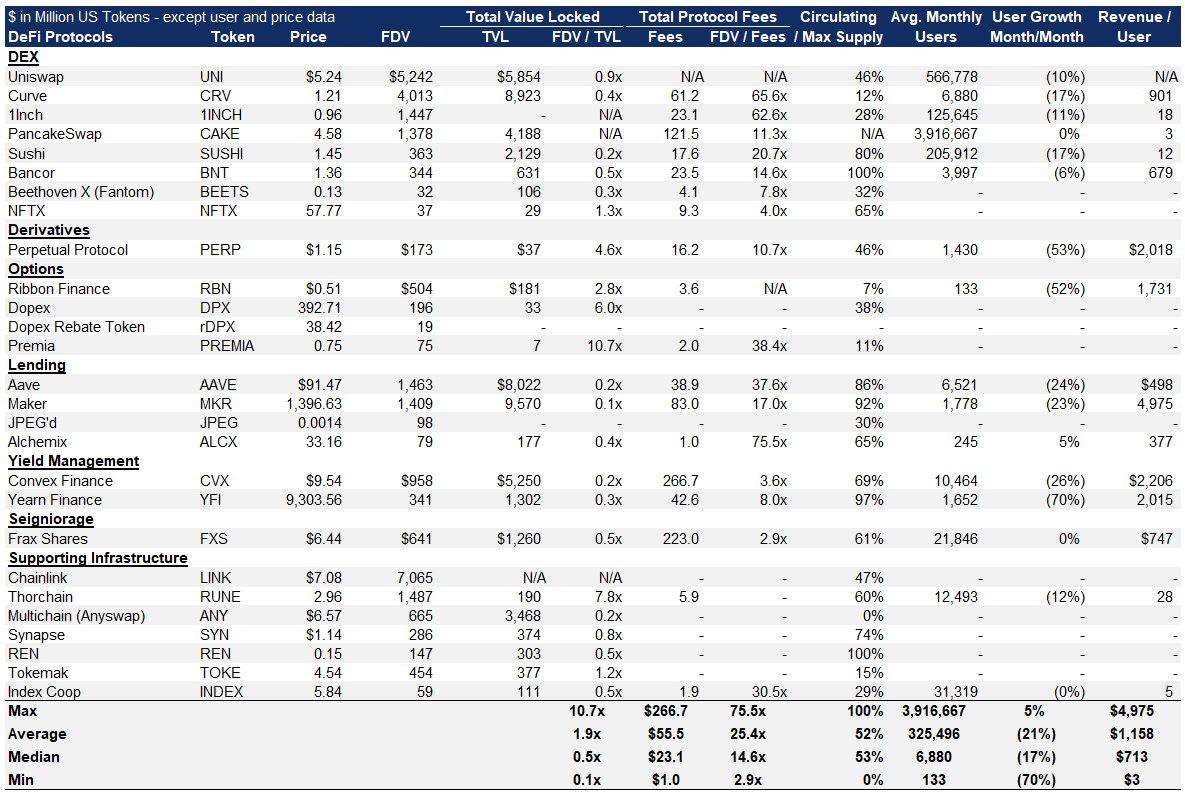

Lending

This segment is most sensitive to interest rate spreads. A good proxy for crypto interest rates is the Bitcoin or Ethereum futures term structure. The cost of carry represents how much traders are paying for leverage.

For much of 2021, people were willing to pay 10-15% / year to have leveraged long exposure to cryptoassets. BTC and ETH are now down 1/3rd from record highs.

Any investor using 3x or higher leverage and who bought within ~10% of the high has been wiped out completely. Those who invested at better prices or at more conservative leverages since last summer are underwater.

So there is less appetite to go risk on. Lending revenues have compressed.

In periods of consolidation, we look for relative outperformance within a sector.

Lending revenues at Aave have remained stable at just under $40m but FDV/Fees has fallen from 135x to 38x (see our original valuation of Aave for a model). Revenues are down significantly at Maker. This means Maker is losing market share to Aave as yields continue to fall. However, Maker’s token is the only DeFi protocol we track to have outperformed ETH during the last 30 days. This means we’ll be taking a closer look at both businesses.

User activity and TVL in the lending sector is weak, likely a result of falling yields. Aave has retained just 69% of its TVL and Maker DAO 72%. These protocols were averaging 8,450 monthly users which has fallen to just 4,150 users less than a year later.

Conclusion: Demand for leverage will be back when we next have a bull market. So which protocols are likely to attract the most demand / TVL and maintain the best margins? Stay tuned.

DEX

User activity on decentralized exchanges remains strong, averaging 803,000 Monthly Active Users across each of the top six protocols we track. Unlike demand for leverage, we don’t expect trading volumes and fees to be as sensitive to market cycles. In a bear market people still trade (and can be forced to trade).

A swap is still a swap, but some innovation has occurred. The last year has seen the release of Curve v2 and Uniswap v3, and we’ve also covered MEV protection and sourcing liquidity from multiple venues with aggregator products 1inch and Matcha.

Reminder: everyone should be comparing prices with an aggregator before swapping.

We continue to wait for a good on-chain orderbook product which will likely be based on a fast L2 rollup secured by Ethereum.

TVL can’t really be compared like for like without a deeper dive into volumes and the capital efficiency improvements in Uniswap v3. We’ve done the digging and passive yields in excess of risk are largely an illusion now. Curve has too much systemic risk around stablecoin exposure. We aren’t recommending passive LP on any DEX at this time.

Yield Aggregators

We slated Yearn for copy pasta the 20% carried interest model from TradFi. Overhead (staff costs) was allowed to balloon. TVL dropped from $3.7b to $1.3b. We don’t see much room for a high cost middleman as yields compress. A basic borrow/lend platform is superior in a bear market.

Liquidity

An interesting and evolving sub segment of DeFi is liquidity provision / management. We covered The Great Curve Wars last year. The dynamics around using governance tokens to control market maker rebates are fascinating. A protocol, Tokemak, was launched with the high aim of revolutionizing liquidity provision in DeFi. And. Traditional market making firms have entered the chat providing RFQ liquidity which can be accessed on chain by aggregators like Matcha or directly with Hashflow.

We don’t see a clear winner yet but fully on chain central limit order books seem like a good bet when layer 2 rollups mature, and RFQ based liquidity is probably here to stay. We’ve been bearish on the passive LP model for some time as market making is a hard problem and quotes need actively managed (skill) to overcome adverse selection (which is the root cause of impermanent loss).

Infrastructure

We covered Chainlink, the monopoly solving the oracle problem over at BowTiedBull. Our first infrastructure research item here at DeFi Education was REN: a way to port BTC to Ethereum via a lock and mint model (RenBTC token). An interesting concept worth covering but our concerns about the economic model (capital inefficiency) seem to have borne out as RenBTC issuance is around 1/3rd of its all time high.

The main infrastructure products are bridges - we are working with Synapse, a leading cross-chain AMM and bridge. There are other interesting infrastructure products which we believe could have rapid growth in the years to come including decentralized storage and decentralized (cloud) computing. Stay tuned for our deep dives on potential future market leaders.

DeFi Metrics

Total Value Locked in DeFi is now ~$111b, up from ~$92b over the last twelve months. The recent sharp decline is of course caused by Terra going to zero and correlated declines in ETH and other tokens. DeFi TVL growing year over year despite billions in hacks and losses shows the resilience of a decentralized system. TradFi would need state aid to absorb losses of this scale.

This isn’t cope. This is free market working, something we didn’t see in TradFi due to “too big to fail” policies.

Comps

The median FDV / fees ratio in the projects we track has fallen from 17.8x to 14.6x and the mean average has fallen from 37.9x to 25.4x. Average monthly users on the median project is fairly stable around 7,000 unique wallets/month +/- 10%. Valuations are down but usage is fairly steady.

We see a modest compression in revenue per user which is to be expected due to competition and greater price sensitivity from users now that the easy times are over.

Price Performance

The median DeFi coin has declined 89% from its record high, compared with 60% for ETH, 57% for Bitcoin, and 29% for the Nasdaq composite. The most resilient coins have been Synapse (-77%), Maker DAO (-78%), and JPEG’d (-80%). Maker DAO’s 30 day decline of -19% outperformed ETH (-34%). We are in a bear market across all risk assets and we are researching to identify undervalued tokens.

So What Next?

As we have stated many times in the past, DeFi is inextricably linked with speculative activity in crypto markets. Many tokens have performed poorly not because the products are bad, but because speculation has left the market and many tokenomics are poorly structured. Of all sectors of DeFi and crypto, the parts that interest us most are the infrastructure plays, gaming, and NFTs x DeFi.

We’re researching different protocols now and will be covering deep dives for *paid* subscribers.

Until next time..

This is a free post - if you found it valuable please give it a share!

If you’re reading this and haven’t subscribed yet, join our community below.

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are opinions from an anonymous group of cartoon animals with Wall Street and Software backgrounds.

Surprisingly BNB is also quite resilient.

Right now I'm seeing it at 53% drop from ATH, actually better than BTC/ETH (at this point in time), and in general within a few percentual points

Whatever happened to that Theopatra real estate DeFi thing that had a bunch of BowTieds with pawns in their bios? Didn’t want to FUD their bags, but trying to own real estate while being a crypto anon seemed a regulatory nightmare.