Yields Can Remain High and Quick Market Opportunity Maths

Level 3 - Virgin DeFi Analyst

Welcome Avatar! First of all, thank you for all of your support so far! The questions/comments/suggestions were all written down and we’re balancing out requests with pre-planned analysis. A big thank you to the OHM team for helping us make sure the overview was accurate across the board with an attempt to remain as unbiased as possible (the goal here is to continue with deeper analysis of each sector/coin).

Today, we’re going to address one big picture item that has come up quite a bit “how long can yields stay this high”. Since we’re building out a DeFi specific educational product, this means we think it can last a *lot* longer than most expect. Why?

The yield difference is structural inefficiency between the current financial system and new software enabled financial system.

Step by Step - Without Complex Calculations

Quick review. Banks make money as follows: 1) you put your money inside the bank say $100,000 US Token, 2) they give you interest on this money, call it 0.5% per year = $500 US Token in interest, 3) the bank then uses the $100,000 US Token to loan out to person B buying a home at ~4%, 4) the bank makes $4,000 US Token minus the $500 paid to you which is $3,500.

Fair enough. Here is the problem: the spread is thinner

Using the same example as above we can add a few zeros. Lets add 3 zeros since banks deal with a large number of loans. This means the bank is making $4,000,000 and is paying out $500,000 US Token for a net “profit” of $3,500,000 per year on $100,000,000 worth of loans.

This assumes no overhead. We repeat. This assumes no overhead.

What is the Overhead: The bank has employees, real estate costs, regulatory license costs, computer/software costs, one time events (lost wires, banks being robbed, ATMs being robbed) and more. These costs make the $3,500,000 in earnings a lot slimmer. How much slimmer? We can take a look at retail banks. Since we *DONT* want to make this complicated, we can use Wells Fargo (LINK to list of largest retail banks). There is no way to choose the ideal bank, however, JP Morgan, Bank of America and Citibank have huge investment banking revenues (high margin, not related to standard lending). Wells Fargo does not have a huge investment banking arm and is more retail focused. Therefore, we’ll use their income statement and ignore all the fines they got over the past couple of years.

Link to Financial Statement (2020, 2019, 2019 from left to right) from SEC.gov

Back to the Quick Math: The $4,000,000 US Token they earn from the 4% loan is reduced by: 1) the $500,000 they pay customers for the deposits, 2) all personnel costs, 3) all occupancy costs, 4) equipment and 5) the other services/advertising costs. As you can see, the 2020 number had a ton of restructuring and other charges so we can look at 2019/2018 instead (revenue and income highlighted in green). Divide the two and we get to the following ratio: 23.5% for 2019 and 26.5% for 2018, to keep it simple we can call it 25%.

Conclusion: The $4,000,000 equals ~$1,000,000 in actual profit. Therefore if they are lending at 4% they are only seeing profits of 1%. That’s it! The rest is costs and other expenses.

Compare to this to decentralized finance? The $4,000,000 would equal around $3,500,000 in profit minus some costs for the people/machinery so at minimum $3,000,000. This means the yields on DeFi should be 3x larger than traditional finance. ($3M US Token/$1M US Token) = 3x

In short, due to an improved business model, the yields should be higher for a long period of time as long as traditional financial infrastructure has overhead costs (people, branches, ATMs, computers etc.).

Some Cold Water to Remain More Neutral

While we’re bullish on DeFi over the next several years, the current state of the market is the wild wild west on steroids dripping with triple ponzi scams, rehypothecation and DeGenerate “traders” who enjoy losing money for one reason or another. This is a long way of saying, most of these projects are just ponzis where money is “given out” to incentivize people to use the project.

Current State of DeFi: The extremely high yields you’re seeing is a combination of 1) aggressive incentives and 2) extremely degenerate bets. Most of the big yields are scams without a doubt. Creation of fake coins with no utility/value and making the price go up.

The second part is a lot more sustainable. While you shouldn’t trade with immense leverage, asking if people will “do it” is a different question. This is like investing in fast food companies. While you shouldn’t eat fast food, it does not mean the average person has the same amount of will power.

Massive Dislocations: If you have crypto assets on multiple chains you can take advantage of volatility. Smaller projects can have imbalanced pools, pegs for “stable coins” can go to 0.95 or 1.05 and create immediate returns. This is something that should decline over time. However. Today, the changes are so rapid that you can quite literally do this without any infrastructure. In the near future, machines will be programmed to do this. Until then, take advantage of the internet money dislocations!

Rugs and “Stolen Funds”: Everyone gets rugged. One of the major benefits of traditional finance is the legality of running off with money. In the Web 3.0 anon world you’re trusting complete strangers. Or as Warren stated “Shadowy Super Coders”.

In the end, the ones with long-term belief systems will build Decentralized Finance ecosystems. They will become wealthier by many magnitudes in comparisons to the scammers who rug pull for a few million US Tokens. The rug pulls are simply the price of admission.

Besides. The majority of the people reading this dropped $50,000+ on a piece of paper that isn’t used for earning an income. The original “rug pull”. Thanks for the tuition!

Long-term Consequences and more Maths

Why in the world would you want to be involved with ponzis, rug-pulls, ultra high yields and competition with traditional finance? Easy! You want to be ahead of the curve and have a bright future.

Think about it like this. If for some reason lending rates go up 5-6%… all this means is that Traditional finance sees a *slight* increase in Net Income margins. While the profit margins may go up a bit, the distance between the two doesn’t change much.

In a second scenario where rates go negative… this means individuals would begin pulling capital out. As capital comes out it has to go somewhere and you only need a fraction of the pie to move into DeFi.

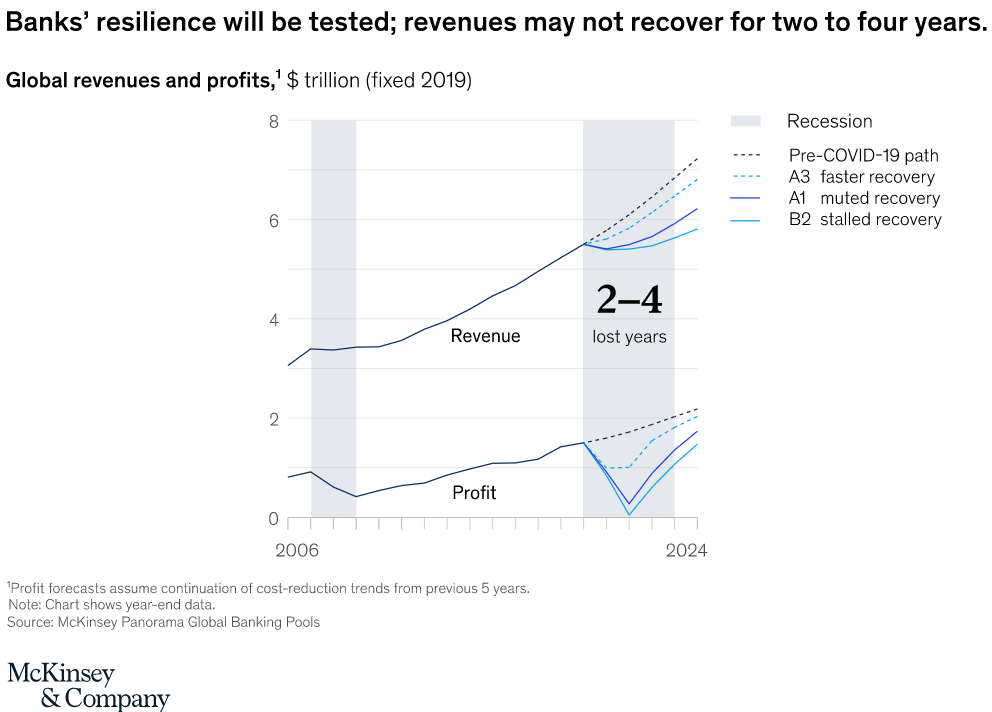

Take a look at the below revenue line for global banking. ~$5 Trillion US Token. According to McKinsey. We know for sure that the projections won’t be right (the historical numbers were checked 100x so we have confidence in those)

Maths: 1) ~$5 Trillion US Token revenue and 2) this should be ~$1.25T US Token Net Income. Since DeFi should be a 3x improvement due to zero overhead, it means the DeFi market alone should be worth $3.75T.

Autist Note: There is no way that this is "correct”. We can cut out $750B for good measure, yet, the point stands. If you zoom out, the opportunity is many multiples of where we are today. The DeFi Market is only ~$120 billion (LINK). Meaning that the opportunity is $3.75 trillion/$0.120 Trillion = 31 times larger!

Something to think about. We’re certainly early!

Disclaimer: None of this is to be deemed legal or financial advice in any way shape or form. You are reading opinions from an anonymous group of Wall Street and Tech Engineers in Cartoon format.

And the 31x is net income vs market cap! We are early

Thank you for writing this. I have around 6 figures of student loan debt and every time I read your blog and get more of your insights, I feel a bit better about myself and smarter each time