8 Projects to Watch in Tokenized Assets

Level 3 - Virgin DeFi Analyst

Welcome Avatar!

We’ve got even more coverage on tokenization this week. If you haven’t already read our primer, go do that now! Last Thursday for paid subscribers we also published a deep dive on FIGR, a company that is up over 100% since it’s IPO 3 months ago and remains ignored by most crypto participants.

Today we’ll break down even more projects and companies operating in the $35B+ space. TradFi firms are continuing to invest in this sector (lots of job postings!).

Ethena USDe - Tokenized Hedge Fund

Ethena is essentially a tokenized hedge fund with a mandate to engage in basis trading strategies across crypto exchanges. The USDe stablecoin represents shares in the fund and accrues yield if the fund earns a positive return. Investors are exposed to risk if the fund / strategy loses money.

Let’s walk through an example of exactly how Ethena works.

You begin with a certain amount of dollars. Let’s say $3 million.

Ethena uses this capital to buy 1,000 ETH, assuming an ETH price of $3,000 per unit.

Ethena mints their USDe stablecoin equivalent to the value of the ETH purchased (in essence, your initial dollar investment is turned into their stablecoin).

A portion of the ETH bought is staked at around 4-6% per year.

The remainder of the ETH is transferred to custodians who work with centralized exchanges, ensuring safe storage and management of these assets.

Ethena opens futures contracts to sell 1,000 ETH across five centralized exchanges (Autist note: A futures contract is an agreement to buy or sell an asset at a future date at a predetermined price). This locks in the sale price of ETH, hedging against future price volatility.

In essence, you give Ethena ETH, which they use to 1) stake and 2) sell futures.

Ethena is one of the most successful crypto products by TVL/AUM and by revenue, and currently manages $6.5B (down from a recent peak of nearly $15B). The basis trade strategy is sensitive to the demand for leverage and doesn’t significantly outperform the risk-free rate in bear or sideways markets.

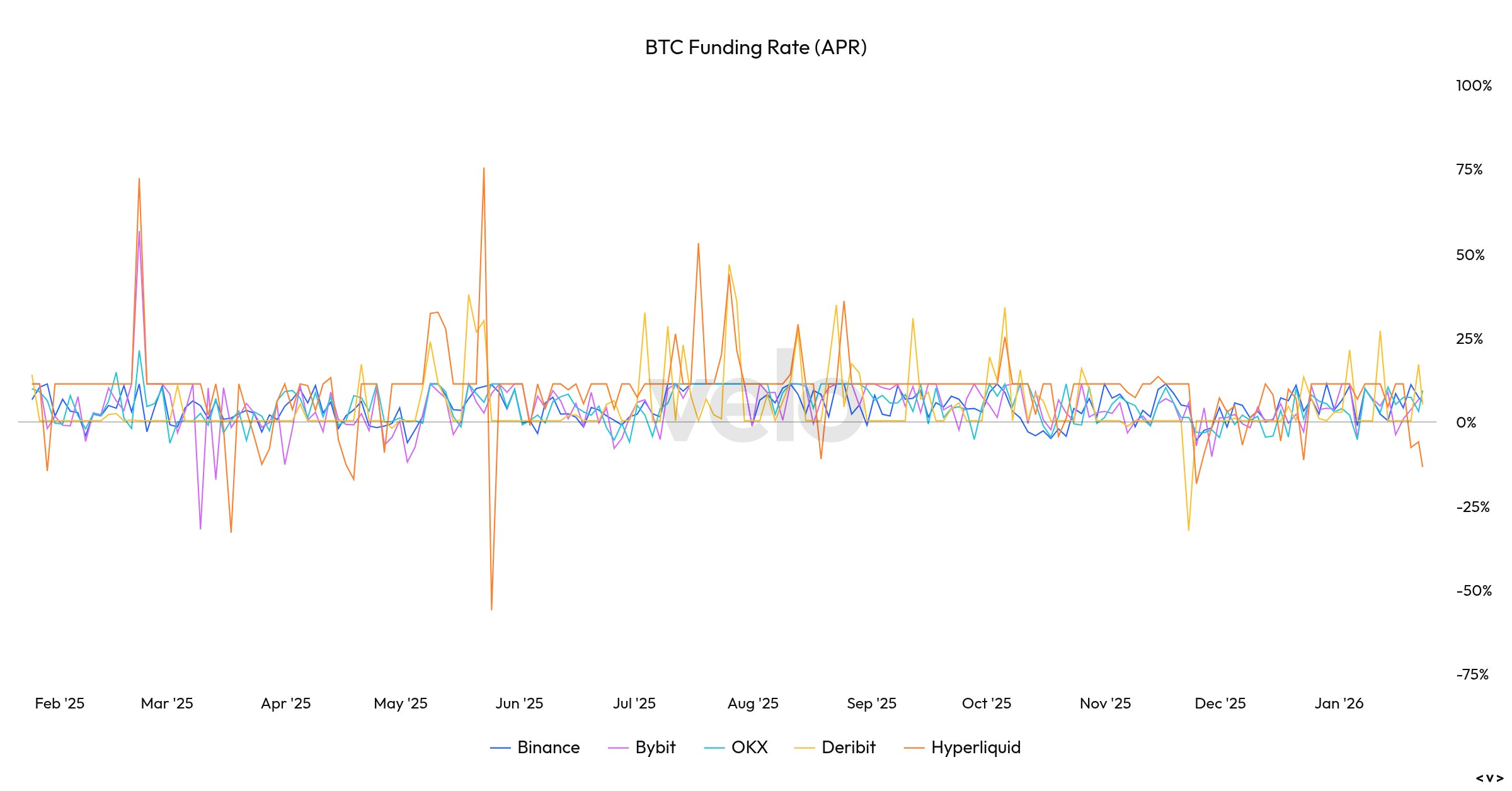

Although altcoin funding rates have been low, there has still been some good cash and carry yield opportunities in select coins. A major fund like Ethena is capacity constrained and essentially limited to trading the majors on very liquid venues.

The carry on Bitcoin has been pinned between 0-10% on major venues for ~1 year. Average realized funding is now 5.6% translating to a 4.9% 30-day average APY on the staking token, sUSDe. This small spread above the risk free rate doesn’t compensate investors for multiple layers of risk inherent in trading activities and is the likely cause of record protocol outflows.

Ethena’s product suite has expanded to include a fund backed ~90% by BUIDL.

On the regulatory front, in April 2025 Ethena was forced to withdraw from the European Union and wind up its German entity after local regulators cited MiCA non-compliance violations, inadequate capital reserves, and potential securities law violations (offering sUSDe without a prospectus). Trading in USDe tokens on the secondary market is no longer permissible in the European Union.

These regulatory decisions aren’t surprising to us. In earlier coverage we’d highlighted what we considered to be some sleight of hand in Ethena’s marketing.

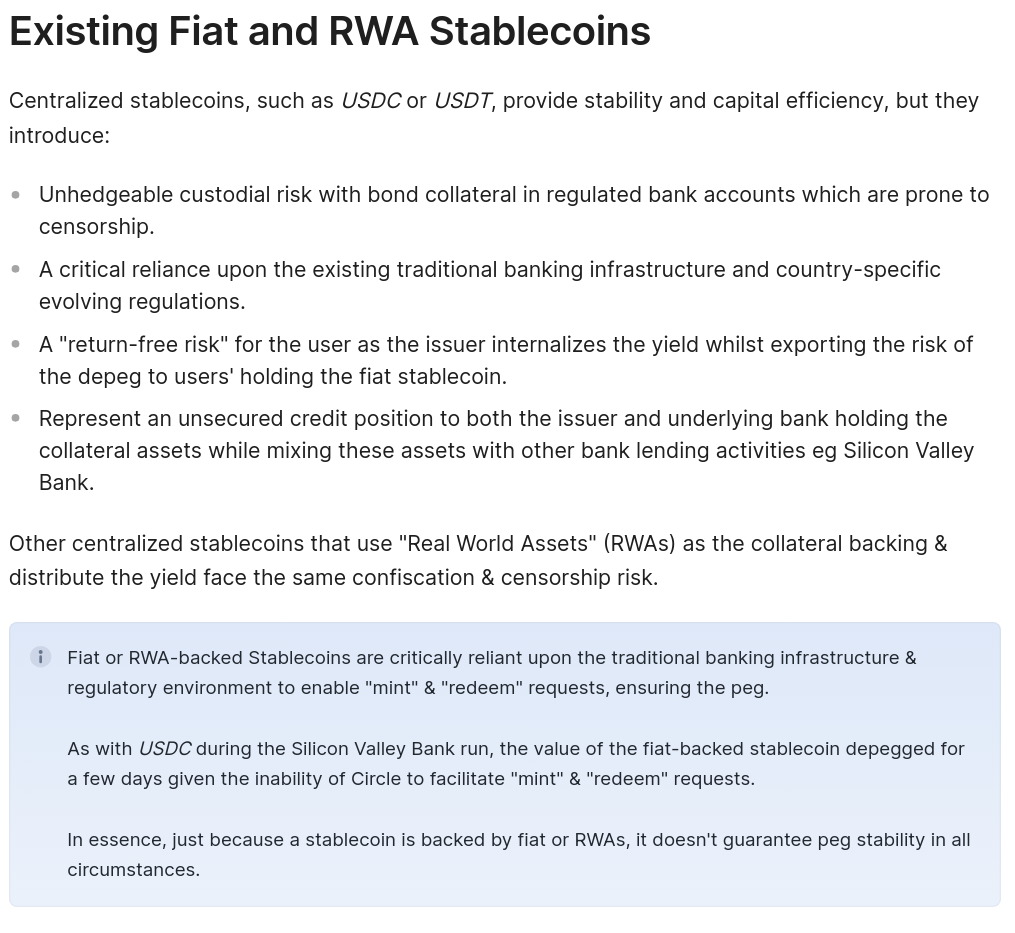

Ethena’s docs helpfully explains why fiat backed stablecoins are risky as part of the value proposition for their tokenized hedge fund stablecoin:

What Ethena’s risk disclosure documents don’t make clear enough - in our opinion - is that profit and loss from its derivatives positions are denominated in these stablecoins.

In simple terms if ETH is at $10k and you own $3b ETH and are short $3b ETH-USDT you have exposure to $3b of … USDT. If the market crashes down 50% in one day you have $1.5b of ETH and +$1.5b USDT P&L for a total of $3b. But. If the market crashed because Tether was insolvent, you have 1.5b USDT tokens which may be worth less than $1, and therefore your position is worth less than the $3b you originally invested. We’re not predicting that Tether will fail, only stating that Ethena inherits risks from USDT in much the same way that DAI inherits risks from USDC.

Following withdrawal from the EU, Ethena operates through BVI entities and excludes US and EU persons from directly minting their stablecoin.

As basis trade returns have compressed both the scale and demand for Ethena’s strategy is limited, and competition from TradFi should further compress the basis trade. Ethena proved the concept of tokenizing a trading strategy but has probably past its peak in terms of absolute TVL and in market share.

BlackRock BUIDL

BUIDL was one of the early funds that provided credibility to tokenization. It was launched in March 2024 as BlackRock’s USD Institutional Digital Liquidity Fund, and has captured $1.68B in assets (down from a LTM peak of $2.9B).

The fund consists of tokenized treasuries deployed across 9 blockchains, custodied by BNY Mellon with Securitize as the transfer agent.

The $1 NAV per token is maintained through a mechanism which distributes yield as newly minted tokens to users’ wallets onchain.

BUIDL is accepted as collateral on venues such as Deribit and and Aave, and fees are that are generally 50bps, with 20bps on certain blockchains that subsidize using their ecosystem funds.

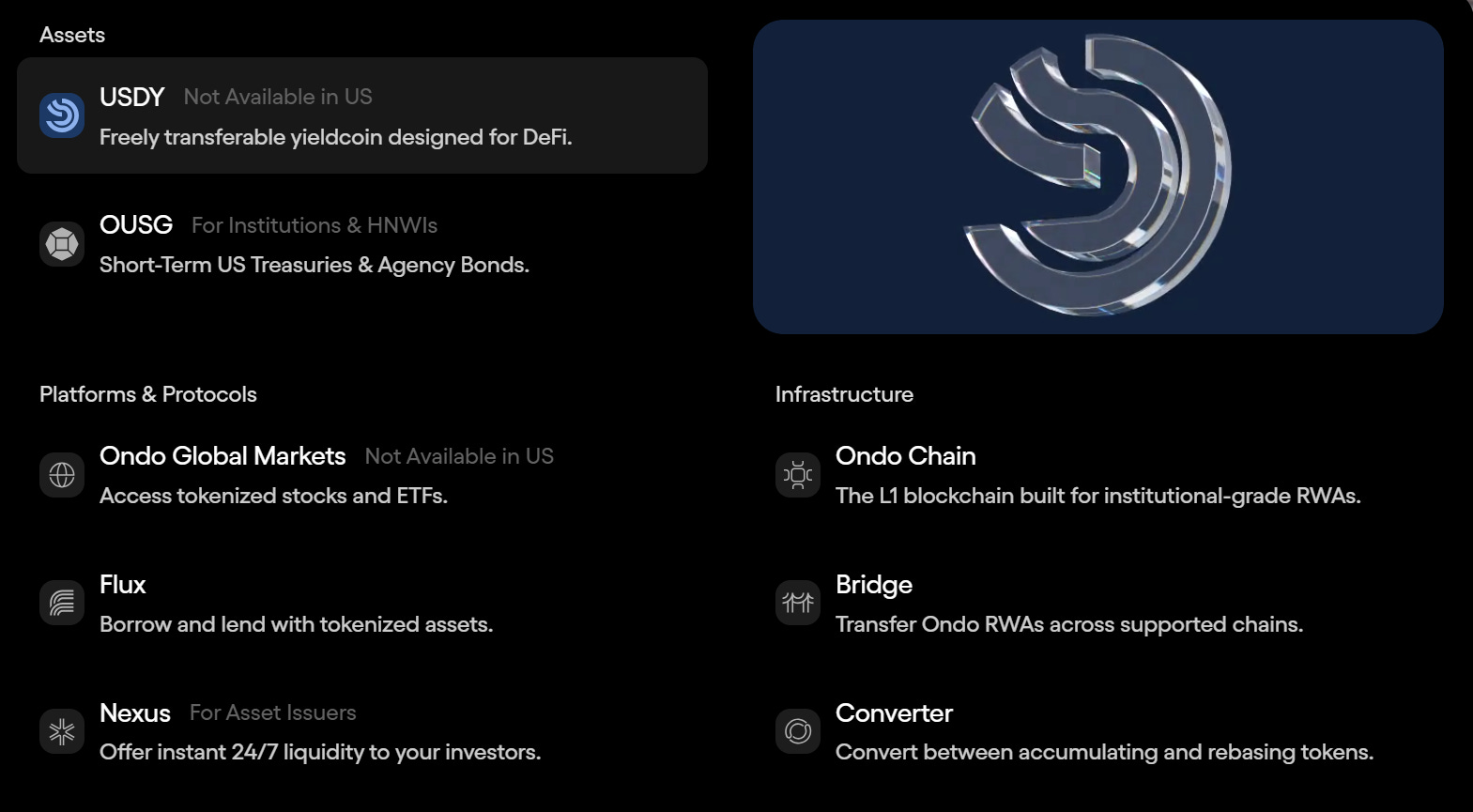

Ondo Finance

Ondo is one of the leading tokenized treasury platforms that was designed from inception for DeFi composability, reaching $2.5B TVL across its product suite. In December 2025, the SEC dropped its Biden-era investigation into Ondo and its tokenized assets with no enforcement action taken.

Ondo’s flagship products are its yield-bearing cash equivalents.

US Dollar Yield (“USDY”) is a permissionless, yield-bearing stablecoin alternative for non-US retail investors. It requires KYC, but no accreditation. USDY is secured by a portfolio of short-term U.S. Treasuries and bank demand deposits. USDY passes the yield to you instead of pocketing it like USDC/USDT.

Ondo Short-Term US Government Treasuries (“OUSD”) is a tokenized fund that provides exposure to U.S. Treasuries. It’s backed by BlackRock’s BUIDL fund and other institutional funds from managers like Fidelity and Franklin Templeton. It requires Qualified Purchaser status ($5M+ investments). The 0.15% management fee is waived until July 2026 as Ondo prioritizes growth over monetization.

There’s also the Ondo U.S. Money Market Fund which is a tokenized U.S. government money market fund.

As is becoming a major theme across protocols and crypto companies, Ondo Global Markets was also formed to compete in the tokenized securities market. Ondo also aims to capture lending and bridging internally through its Flux Finance and Ondo Bridge that allow people to use OSDY and OUSG.

Tokenized Gold

The tokenized gold market has surpassed $5.1B in total market capitalization, a record high driven by gold prices breaking the $5,000/oz threshold on-chain. The market is led by Tether Gold (XAUT) at approximately $2.6B and Paxos Gold (PAXG) at roughly $2B. While both assets offer 24/7 liquidity, they represent fundamentally different regulatory and operational philosophies.

Paxos operates under a strong regulatory framework in tokenized commodities. The New York Department of Financial Services approved PAXG as the first regulated gold-backed virtual currency in 2019, and Paxos received OCC National Trust Charter approval in December 2025. Monthly attestations from KPMG verify 1:1 backing with LBMA-certified gold bars stored at Brink’s London vaults. Paxos charges no custody fees and tiered creation fees from 0.125% to 1.00%.

Tether Gold offers comparable economics with zero custody fees and 0.25% create/redeem fees, but operates from El Salvador under its Digital Asset Service Provider (DASP) license. Tether disclosed in July 2025 that it owns its Swiss vault storing approximately 80 metric tons of gold.

Tether’s quarterly BDO Italia attestations draw criticism compared to Paxos’s monthly KPMG audits. Both require 430 tokens minimum for physical gold bar redemption, though Alpha Bullion offers smaller PAXG redemptions down to 1 gram.

Franklin Templeton: SEC-registered on-chain funds

The Franklin OnChain U.S. Government Money Fund (FOBXX) achieved a regulatory milestone in April 2021 as the first SEC-registered mutual fund to use public blockchain for share ownership records. Current AUM stands at $766 million.

Franklin’s approach differs fundamentally from offshore competitors by operating as a fully compliant 1940 Act fund subject to Rule 2a-7 money market regulations. This means no Qualified Purchaser requirement - retail investors can participate. Also:

Full SEC prospectus disclosure and audit requirements (PwC serves as auditor)

J.P. Morgan custody for underlying securities

Daily NAV at $1.00 per BENJI token

The fund’s 10-blockchain deployment includes a proprietary transfer agent system built in-house. A June 2025 upgrade introduced patent-pending intraday yield calculations to the second-enabling precise yield attribution for short-term collateral use cases.

Total expense ratio after fee waivers is 0.20%. The Canton Network integration with HSBC, BNP Paribas, and JPMorgan for institutional collateral represents a significant TradFi bridge among tokenized products.

Superstate

Founded by Compound Finance creator Robert Leshner, Superstate manages ~$1.3B in assets across two products designed specifically for DeFi composability while maintaining SEC compliance.

Short Duration US Government Securities Fund (“USTB”): Holds ~$820 million AUM with a 0.15% management fee and targets Qualified Purchasers. The product features continuous pricing with real-time interest accrual, which enables 24/7 NAV without traditional fund accounting delays.

Crypto Carry Fund (“USCC”): At ~$440 million AUM, this fund employs basis trading strategies similar to Ethena but as a regulated fund. The 0.75% management fee reflects active management, with returns reaching 8–10% during favorable funding rate periods (currently yielding an implied 5.8% at time of writing).

Assets are held through Anchorage Digital Bank (federally chartered) and BitGo. Notably, Superstate Services LLC was officially approved as an SEC-registered transfer agent in March 2025, allowing the firm to launch its “Opening Bell” platform for on-chain public equities.

Key Differentiators:

Aave Horizon integration enabling USTB/USCC as collateral for borrowing USDC, GHO, and RLUSD.

Frax Finance approval for frxUSD collateral backing.

The $100,000 minimum investment and Qualified Purchaser requirement limit retail access.

Centrifuge

Centrifuge has evolved from its early invoice tokenization roots into a $1.2B TVL platform supporting institutional-grade structured products. The August 2025 milestone of $1B TVL placed it alongside BlackRock/Ondo and Figure as among the first Tokenized Asset platforms to reach that threshold.

The protocol’s partnership with Janus Henderson (managing $400 billion in traditional assets) produced three major products:

Centrifuge requires Accredited Investor status for U.S. participants.

In July 2025, Centrifuge completed its v3 migration, moving to Ethereum, Base, Arbitrum, and other EVM chains.

Circle USYC - Money Market Fund

Circle’s January 2025 acquisition of Hashnote for approximately $100 million instantly positioned the USDC issuer as operator of a top-tier tokenized money market fund. Current AUM is ~$1.69B. The strategic logic is enabling institutional clients to move between stable cash (USDC) and yield-bearing treasuries (USYC) through a single API.

USYC tokens represent shares in the Hashnote International Short Duration Yield Fund, a Cayman Islands registered mutual fund investing in T-Bills and reverse repos. Yield accumulates through price appreciation (currently ~$1.11 per token).

The fee structure is:

10% performance fee on yield generated

0% subscription/management fees

0.05% redemption fee

Available exclusively to non-U.S. persons under Regulation S, with a $100,000 minimum. Integration includes the Canton Network for TradFi connectivity and Deribit cross-collateral support (with a 10% haircut).

Concluding Thoughts

Crypto-first institutional products like Circle’s USYC are outcompeting TradFi products like BlackRock’s BUIDL in terms of liquidity and AUM. The market is choosing assets that integrate seamlessly with onchain markets over those with “Qualified Purchaser” barriers.

The resolution of the SEC’s multi-year probe into Ondo Finance signals a “regulatory ceasefire” that is giving other issuers the confidence to move beyond simple Treasuries. We are entering an era where onchain is becoming a layer that provides universal collateral. Yield-bearing gold, tokenized S&P 500, treasuries, etc can all live in the same wallet and be transacted 24/7, instantly. Much of these developments, like Figure, are being completely ignored by crypto natives.

For our subscribers, the *key takeaway* is that crypto’s Tokenized Asset subsector is no longer about if tradfi assets will move onchain, but about which protocols and companies will win the race to become the industry’s main asset originators, providers, and sources of liquidity.

Wall Street 2.0 is coming and we are still in early stages.

Join the paid subscriber list to receive our next research report this Thursday and our next DeFi Roundup on Saturday.

Paid subscribers get access to:

All of our past posts

Weekly Deep Dive Report

A comprehensive bi-weekly DeFi Roundup

Bi-weekly Q&A sessions with our team

Until next time..

P.S. If you’re having a hard time keeping up, join the Academy to understand the core frameworks we use in our research process at a fundamental level.

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are opinions from an anonymous group of cartoon animals with Wall Street and Software backgrounds.

We now have a full course on crypto that will get you up to speed (Click Here)

Security: Our official views on how to store Crypto correctly (Click Here)

HEAT