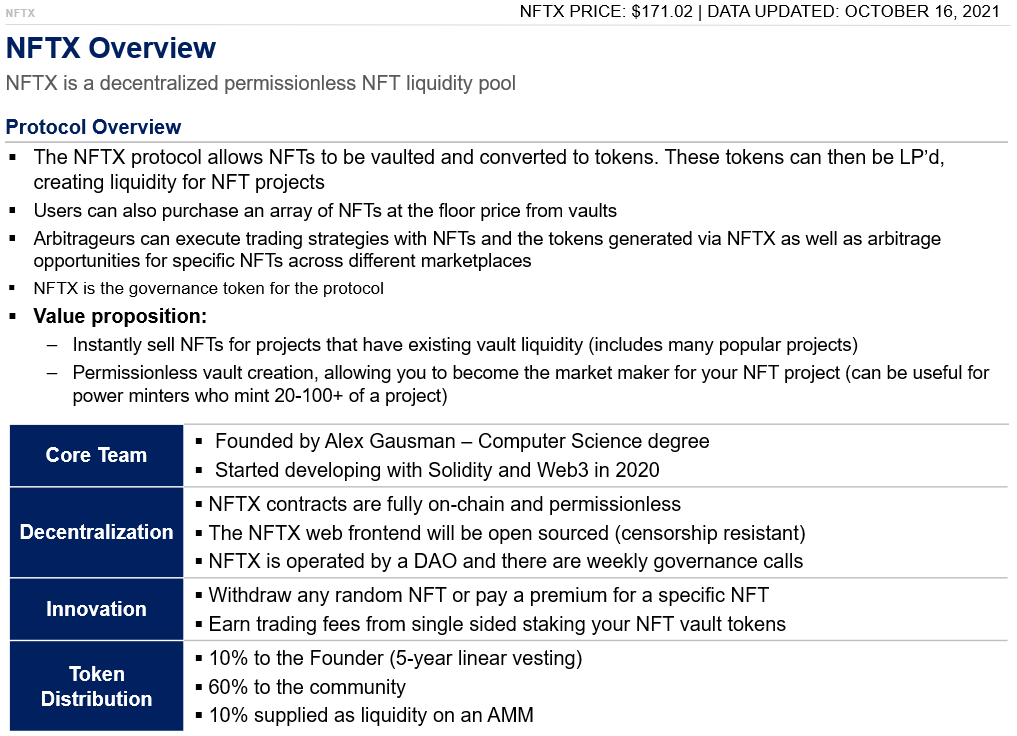

NFTX Overview

Level 3 - Virgin DeFi Analyst

Welcome Avatar! Today, we have an overview of NFTX. We’re sending this out to all so new subscribers can get a glance of how we structure a basic overview of a token. Most projects we look at have earnings/valuation methodologies however, NFTX does not have a clean way to value it (future is based on innovation vs. current token earnings).

Intro Questions

Why use NFTX? NFT owners can deposit their NFTs into a vault for that project on NFTX and mint a token (vToken). This token represents a claim on an asset inside that vault. When the owner redeems, the token is burned and a random NFT from the vault is returned to the owner. Specific NFTs can be redeemed for a fee.

NFTX offers exposure to the “floor” of an NFT collection, the main advantages are instant liquidity (AMM pool) rather than waiting for a counterparty for the specific NFT, and ability to transact in sizes smaller than 1 NFT unit (e.g. investing in a fraction of a floor Punk). NFTX essentially transforms a Non-Fungible Token into a Fungible Token which can benefit from increased liquidity and lower trading costs.

Another benefit is the ability for NFT owners to become liquidity providers and earn yield on their tokenized floor NFTs. In the future, NFTX plans to provide single-sided staking yield thereby unlocking the value of floor assets. We highlight floor assets because any staked NFTs can be purchased through the vault. As such, users should be extremely careful to not deposit rare NFTs into a vault.

For example, as of the time of writing, a Hashmask can be purchased from an NFTX vault for 1.31 ETH. If a clown Hashmask was to be deposited into this vault, it would be purchasable for the same price. The NFTX vault views *all* NFTs within a project as the same (makes NFTs fungible). That also means the reverse is true – if you find a rare NFT inside a vault you can claim it and relist it on another marketplace for a rarity arbitrage™ (Owl once made a 2ETH profit this way in one evening – while this is unlikely to be a frequent occurrence, there may be opportunities to play mid to upper mid tier rarity NFTs more frequently and capture smaller profits from people who simply want quick liquidity).

The recommendation here would be rather than scout every vault for a rare NFT, pick 2-3 projects you are familiar with already and check in on the vault every so often as there may be a rarity arb opportunity! While there is no reason for this to be a dominant strategy, it can be a fun and relatively simple way to make a quick profit.

What are the other options and how does NFTX differ? Other NFT liquidity pools include:

NFT20: Same concept as NFTX; has a token called MUSE. We prefer NFTX because it is more intuitive to use and relatively easy to understand for the average NFT person. However, MUSE token can accrue value through trading fees, which is superior to NFTX’s token which has no value accrual mechanics at the moment.

Unicly: NFTs can be tokenized and traded. These tokens can be LP’d and staked to earn xUNIC tokens. Seems to target the Asian market. We find Unicly clunky and difficult to understand and use. We believe the UI/UX will be a significant deterrent to adoption.

What are the costs of using NFTX? V1 did not charge any fees. V2 allows vault creators to set fees based on minting and redeeming vault tokens. The default fees are 5% to mint, 5% to redeem a specific NFT, and free to redeem a random NFT. Anyone providing liquidity can bypass minting fees.

Fees/Income: 1) How does NFTX make money? Protocol revenue has not been turned on. In the future, governance can elect to earn revenue; 2) How much does it make per revenue stream? None currently.

Ownership

1) Who owns most of NFTX? Token distribution is: 10% to the Founder (5-year linear vesting); 60% to the community raise (breakdown here: LINK): 10% supplied as liquidity on an AMM; 20% held in treasury and used for market making activities;

2) Top 10 wallets or estimate? Protocol wallets, Sushi pool, and some unknown wallets one of which might be the founder.

3) Incentives for people to use (or provide supporting infra)? LP fees to provide liquidity in pools, that’s all for now.

Risks

Competitive Risk Many highly competitive NFT marketplaces will be launching in coming months, including Sushi’s Shoyu marketplace and Coinbase NFT. Given the resources behind some of these projects, NFTX’s model may get copied and/or disrupted (especially Shoyu since it is being created by Sushi, an AMM)

Potential mitigant: We do not consider NFTX to be an “Opensea Killer”. Instead, we believe NFTX can be successful as a complementary protocol to other marketplaces. We would be more concerned if Shoyu and Coinbase took the liquidity pool approach and would reevaluate at that time

Tokenomics

No value accrual mechanics currently for the NFTX token. As such, owning the NFTX token is a bet that there will be future accrual mechanics included. Per the usual, the DeFi team heavily discounts future promises on value accrual

Potential mitigant: Potential for future value is a judgment call. Based on our brief interactions with the team, the fair distribution of tokens and the long vesting period for the founder, we are cautiously optimistic as opposed to writing the token off entirely

Software and Security

Software Quality, Audit, and Exploit History: NFTX v1 was audited by Code 423n4 in June 2021. Additional logic was added after the audit was complete, leading to an exploit in which 2 CryptoPunks were stolen the following week

As Punks pre-date the ERC-721 standard, NFTX had implemented some custom logic to transfer the Punks, and omitted a check that the transfer function should only be called by the owner. This was promptly fixed (and NFTX repurchased the stolen Punks on the open market).

The protocol used to be vulnerable in theory to an attacker subverting the process to withdraw a random NFT in order to withdraw a chosen (potentially more valuable) NFT from the pool, but this is moot since v2 when users can withdraw a specific NFT on payment of a premium

Trail of Bits audit is scheduled for Q1 2022

Previously the code had been under heavy development but now there are not many changes to the core vault code, which reduces the likelihood of bugs being introduced

The team has not disclosed any formal software development or quality assurance protocols in use at NFTX – they “test in prod”. There is an active Bug Bounty program (up to $50,000 for a critical bug)

Summary: A new protocol under active development without a current software audit or insurance coverage is at the riskier end of the spectrum, but this is not unusual

Insurance: Not currently available as most providers demand a current audit, team will prioritize accessing cover from Nexus Mutual when the Q1 2022 audit is complete

Owl and Iguana Opinion / Holdings

Brain: Has the view that you’re better off owning high-end NFTS. If we look at the price performance of high-end NFTs (Bored Apes/Toadz/Punks) the higher end units seem to go up significantly more than the protocols/projects. Since it isn’t possible to invest in Opensea it’s better to own the high-end NFTs and wait for a successful decentralized Opensea to pop up. Also as mentioned here, it is better to look at the vaults for a better risk adjusted return.

Iguana – tiny position, < 2% of holdings, follower of Owl’s thesis that it could pivot to an NFT trading venue, and this hadn’t been priced in.

Owl – Tiny position as well. Love the concept and I think they have the best / easiest to use UI/UX of the NFT AMMs (far more important for NFTs than DeFi). The market seems to agree as they have the most NFTs compared to competitors. However, the token is a valueless governance token, hence the small position.

That being said, NFTX is still an early stage startup and I believe the team is genuine when saying governance can vote for value accrual in the future. The founder also has five-year linear vesting on his tokens, which is rare to see in crypto and demonstrates long-term alignment with the protocol. Token distribution overall is fair. As such, I’m willing to overlook the valueless nature of the governance token today. I’m managing my risk by only putting on a small position. If they become the dominant NFT AMM, a 10-20x is in the cards. If there is too much competition and it goes to zero, I wouldn’t lose any sleep over it.

Once single sided staking goes live, I will look to NFTX to stake my NFTs. I think single sided staking could be a catalyst that could cause NFTX to moon quite a bit (assuming competitors don’t get it done first!). LPing NFT-ETH isn’t that appealing to me personally due to IL risk.

Sources Used: 1) Price and volume data powered by CoinGecko API; 2) Protocol volume and User data – Dune Analytics (NFTX)

Disclaimer: None of this is to be deemed legal or financial advice in any way shape or form. You are reading opinions from an anonymous group of Wall Street and Tech Engineers in Cartoon format.

Didn't know where else to write this, so a bit off topic. I would like to find a way to quantify changes in momentum, either to the upside and downside. I saw a linked article on CT to: https://insights.deribit.com/market-research/momentum-bitcoin-and-reflexivity/

Here they use Hurst Exponent to assess price momentums, which could be pretty important in helping to determine when to get in, or more so, when to get out. I pulled 4yr, day to day, historical data on Eth price from Coingecko, and ran the analysis in R (~0.9, very reflexive, no surprise).

1) What are your thoughts no this tool?

2) I am having trouble accessing the hr-hr price data. If I only have day2day price data, the minimum time frame is ~20days. Thus, to do more intra-month analysis (which I think is critical since price/momentum moves very quickly), I need hr2hr price data. Can anyone help there?

Ah so $PUNK is a fractionalized medium for punks? Would be great to know all of the ways to purchase fractionalized premium NFTs