Straight Outta DeFi - R.W.A

Level 3 - Virgin DeFi Analyst

Welcome Avatar!

Today’s post is about R.W.A.. Real World Assets, a 100x+, multi-trillion dollar market opportunity with large scale implications for crypto markets and financial markets at large.

Real World Assets are the utopian vision of blockchain technology. A world in which all things of value are on-chain in some way is

Consensus is that RWA are many years away. In this article, we’ll go over why they might be closer than you think.

Crypto’s Relationship with Speculative Activity

One thing we came across early on when while digging deep into the value drivers and key metrics for DeFi Education is that DeFi protocol growth, revenue and other metrics of adoption are highly linked to speculative activity in markets.

When the market is hot (BTC / ETH going up in price), speculation begins to re-enter the crypto market. People start swapping into alts which generates fees for DEX protocols and liquidity providers. Since investors want to take advantage of booming markets, borrowing also goes up which boosts yields for lenders, fuels protocol earnings and boosts yield farming rewards.

Key takeaway: Rising crypto prices drives market activity which is then captured by DeFi protocols. DeFi and speculation are inextricably linked.

But what happens when prices aren’t booming? Well, people become bored and start to look at other markets to trade. DEXs start to see fewer swaps and there are less fees to go around for LPs. Yields may start to compress or become less attractive in USD and ETH terms as farmed tokens decline in value faster than you can sell them.

These mini boom and bust cycles have become typical of crypto markets in addition to the longer bear and bull markets experienced over the last decade.

Right now, the main connections crypto has to the “real world” (basically anything not crypto) at scale are BTC, ETH and stablecoins. BTC as the decentralized swiss bank account on the cloud, hard money, gold 2.0, etc. and ETH as web 3.0’s decentralized money, oil, etc.

BTC and ETH are not particularly stable assets either, both exhibiting periods of extreme volatility. The impact of this volatility as well as the bull and bear markets spills over to all cryptoassets.

So what in crypto is resistant to speculative activity? We think the two answers today are the following:

Stablecoins - USD stablecoins have significant adoption, with leading stablecoin USDT doing over $60 billion a day in trading volume. The main challenge with stablecoins is that the market leaders (USDT and USDC) do not have a good way for us to get exposure to their usage as an owner (profits are internalized by Tether and Circle, respectively).

Gaming - If/when crypto games are actually good and worth playing for reasons beyond financial incentives, this sector should be more resistant to broader crypto markets. Why? Gamers would continue to play games they enjoy even if perceived ROI were to decrease. This is an area we are watching but we don’t think any game has solved for this (yet).

Real World Assets - Assets from markets that exist completely outside crypto would be subject to the dynamics present in their respective market. Crypto would serve as a vehicle to get exposure (e.g. tokenization).

Today we’re focusing on RWA.

In the near to medium term, we believe RWAs are the answer to “what will be resistant in a bear market”. Crypto markets are highly speculative, as we’ve established. That means we must look elsewhere for uncorrelated opportunities.

RWA Protocols Today

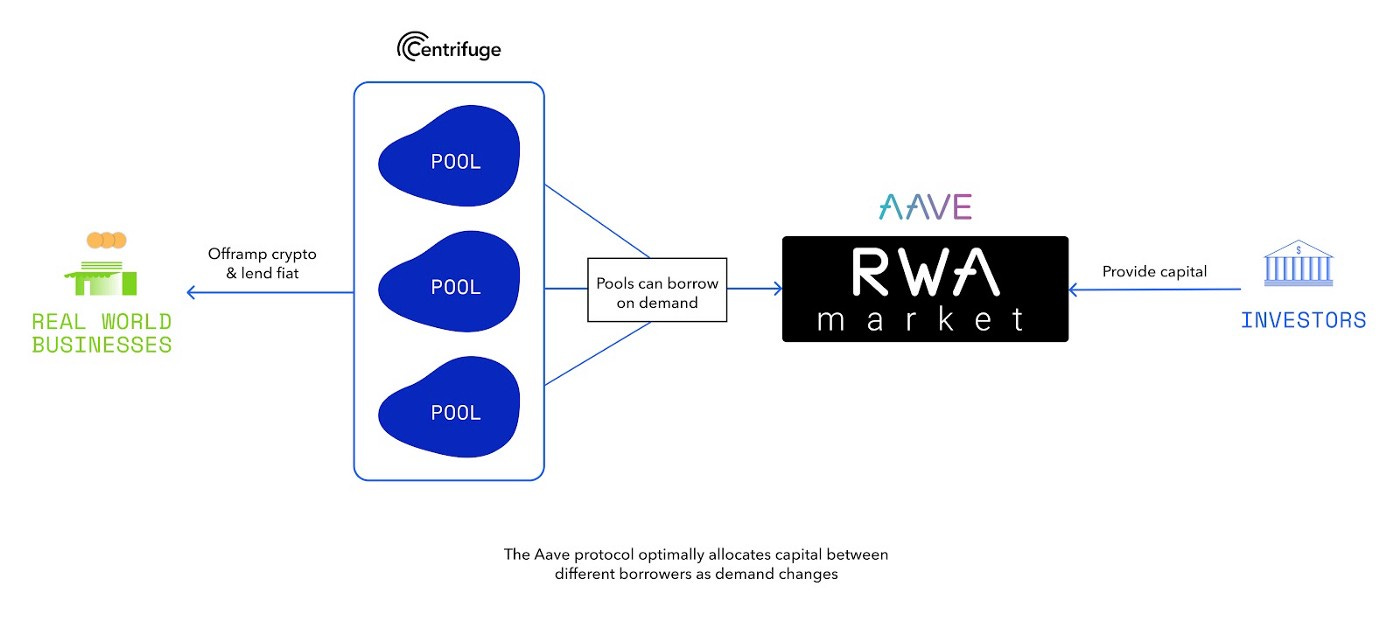

RWA in DeFi right now is primarily centered around lending.

One example is the the Centrifuge “Real World Assets” market on Aave that went live in December 2021. This market allows collateral linked to off-chain cash flows to be pledged to borrow USDC.

Examples of RWA collateral include tokenized Real Estate loans, trade receivables, cargo invoices, and inventory financing.

Investors can deposit capital and real world businesses can borrow. In the case of Centrifuge, they connect DeFi investors (lenders) to “asset originators” aka those providing the asset to borrow against.

To give you a sense of the possibilities in this sector of DeFi, the global real estate loan market alone is over $8 trillion. The global fintech lending market is $500 billion. The commercial lending market is close to $9 trillion.

You get the point. The addressable market for these kinds of assets is massive. In comparison, the TVL for RWA protocols Centrifuge, Maple Finance, TrueFi and Goldfinch Finance combined is under $2 billion.

We are in the very early stages of RWA, but we believe this is one of the core sectors that will unlock the value of DeFi.

Challenges and Considerations

RWA protocols are not without their own unique set of challenges. They may face more regulatory scrutiny than other sectors of crypto because they will be going up against banks and traditional lenders.

RWAs will be at the forefront of banks going to zero.

Furthermore, the degree to which RWAs are decentralized and permissionless is likely to be a point of contention within crypto.

Finally, we think crypto market participants are not well equipped to understand underlying credit risk (DeFi Education is here to help!).

Legal Structures

One of the main opportunities in RWA is creating a ‘back end’ legal structure to efficiently mirror the on-chain transfers of tokens. Remember that the token derives its value from the real world asset and can therefore be impacted by any legal or practical issues affecting the asset.

Real World Assets all come under a legal jurisdiction:

Land - by its location

Intellectual property (tokenized royalty rights) - by where it is registered

Security instrument (e.g. inventory loan) - company location

Economic value accrues first to the legal asset and secondarily to its derivative, the RWA token. This makes the tokenized asset ‘junior’ to legal claims on the RWA it represents. And. Just like stablecoins can become de-pegged, tokens based on RWAs can become undercollateralized in an event which limits token holder’s access to the full economic benefits of the legal owner or which budens the real asset with a debt or fine.

Third party rights and other events could occur which affect the value of the token:

Personal injury of a person on the land leading to a legal claim

Neighbouring landowners acquiring rights over the RWA land or objecting to RWA land use, leading to a legal claim

Pollution or environmental issues leading to government interference with the land, a fine to the landowner; or changes to property tax rates

Insufficient insurance or failure to stay current with premiums then the land is damaged by fire, flood, or natural disaster

Ports and warehouses where physical inventory is stored would have legal priority in attaching and selling the items if they were owed money

intellectual property rights could become the subject of a legal disputeI

The holder of the token representing the RWA would not receive automatic notice of many real world issues which could affect the value of the token. This makes it challenging to set up a liquid secondary market as token buyers could not do much due diligence on any claims against the asset they were acquiring - this problem is similar to “the market for lemons”.

A successful RWA platform will have to be creative in solving this problem, making due diligence information available and working hard to standardize on asset quality.

Big opportunity here.

Permissioned ledgers

It is likely that the first round of RWA protocols to achieve scale will operate on permissioned ledgers for the simple reason that only a permissioned ledger can ensure that all participants have entered into the necessary off-chain legal contracts to make their on-chain activity legally enforceable if required.

We use “documents of title” to confer ownership rights on the owner of land and these rights pass with physical transfer of the document. Cryptoassets are not yet legally recognized as being the type of instrument which can be used to transfer legal ownership in land.

Many difficult legal issues can be avoided by participants agreeing that the ledger will be treated as the definitive record of rights and title as between the participants in that permissioned blockchain system. It remains to be seen how a cross border, anonymous, and permissionless system would operate.

RWAs 1.0 is probably going to require some sort of Master Agreement between issuers and other participants similar to the ISDA rules governing derivatives transactions between banks.

Concluding Thoughts

Despite these challenges, adoption of RWA protocols is gaining steam and represent a huge opportunity for the people who figure out the best working solution and onboard assets to crypto. Undercollateralized lending protocol for institutions Maple Finance has originated over $1.1 billion in loans via its platform to borrowers such as Alameda, Wintermute, and Framework Ventures.

We expect these assets to outperform in bearish crypto conditions as they retain their cash flows due to their predetermined loan agreements.

There are a number of RWA protocols out there. In our next post for paid subscribers, we will be doing a deep dive on various RWA protocols, giving our opinion on who we think might be the lead horse in the RWA arms race and disclosing what we are investing in to get exposure to this sector.

Regardless of the eventual winner, this is a market with plenty of room to exhibit massive growth.

You’ll want to pay attention.

Until next time…

This is a free article. We are a niche research publication building an in-depth fundamental analysis and educational platform to give crypto users and investors better odds against VC Funds, influencers and whales that control the market. We teach you to think like them.

Our publication relies purely on content quality and word of mouth to grow so we would appreciate if you could give this article a share.

In our paid substack, we dive deep into protocols and tokenomics as well as provide broader market commentary. Thousands of readers trust us for our analysis. No frills no shills.

Join our community below.

Disclaimer: None of this is to be deemed legal or financial advice of any kind and the information is provided by a group of anonymous cartoon animals with backgrounds in Wall Street and Software.

Owl is his name and the boys coming STRAIGHT OUTTA DeFi

The OHM Assassinator

Farmin' all night long, call him the Yield Navigator

First you get the 'tism, then you get the paper

Can't chain him down to the buyside, he's got too much $RAIDER

Thanks for the article - I had absolutely no clue this asset class existed. GODSPEED TO ALL DEFI EDUCATION SUBS !