Options for Beginners

Level 3 - DeFi Virgin Analyst

Welcome Avatar! Today we bring you a beginner’s guide to options. Options are derivatives creating the right and corresponding obligation to transact in an asset (stocks, bonds, crypto tokens) at a pre-agreed price.

Options have uses in portfolio hedging and estimating / managing risk as well as providing leverage for degen speculators.

Options trading is growing. Fast.

Options trading in TradFi has exploded. Single stock options volumes were up 68.2% in 2020 compared to the previous year.

Why should you, the astute DeFi investor, care about options? Simple. Sell shovels to the gold rush. Options provide leverage which degens love. No protocol is yet the clear winner so there’s a massive opportunity if you can spot and back the future leading DeFi options protocol(s).

What are options?

An options contract is an agreement to transact on an asset at predetermined price with a defined expiration. Options contracts contain the following information:

Nature of the right – from the option buyers’ perspective, to buy (call) or sell (put) the asset

Specification and quantity of underlying asset (e.g. 1 BTC, 1,000 barrels of crude oil, etc.)

Strike (or exercise) price - the price paid or received for the asset if the option is exercised. This is agreed between the parties – electronic trading platforms organize all the market quotes by chosen strike price.

Expiration date - the last date the option can be exercised.

Rules for exercise and settlement.

In simple terms: Buying call options are a bet on number go up. Buying put options are a bet on number go down. Options have a predetermined expiration. They are derivatives meaning you do *not* own the underlying asset. Rather, you own a contract that represents an agreement for the asset at a defined price.

10 BTC call options with a strike price of $55,000 expiring on December 31st gives the buyer the right (but not the obligation) to buy 10 BTC for $555,000 at any time until the end of the year (American style option).

In comparison, a European style option permits exercise only on the expiration date. A European option is rationally exercised only when it is “in the money” at expiry.

“Moneyness” refers to whether the asset price is above, below, or equal to the exercise price. Calls are in the money (“ITM”) when asset price > strike and out the money (“OTM”) when asset price < strike. Put options are the opposite. Price = strike is known as at the money (“ATM”).

How do I use options?

Options can be used to speculate on the future price and volatility of an asset, and to manage risks in a portfolio. All possible positions are constructed from three basic building blocks:

The underlying asset

Call options

Put options.

You can buy or sell (write) both types of option.

Option Pricing Example: The value of a call option for a non-dividend-paying stock according to the model published in 1973 by economists Fischer Black and Myron Scholes

Owl note: Iguana put this math equation in - don’t be afraid, read on.

Derivatives should be efficiently priced. In other words, there should be no advantage to selecting any type of option or strategy. Most people don’t understand this. Here is why:

The writer (seller) of the option (usually a market making firm) needs to hedge the liability of the option (delivery of underlying asset). Therefore, the cost of the option (the premium) should be equal to the expected cost of hedging over the lifetime of the contract.

Hedging can be done with other options or by buying / selling the underlying asset. This incurs costs, sometimes frequent costs, as the price of the option does not change in a linear relationship with the price of the asset. It is therefore intuitive that:

Longer dated options (more time to expiration) cost more to hedge

Options trading at the money cost more to hedge as they need to be hedged more frequently (can change from in the money to out of the money quickly in response to small movements in the asset price)

Options trading far out of the money do not need hedges adjusted frequently as they have a low probability of expiring in the money

Options in volatile markets should cost more than options in calm markets, because large swings in price create more transaction costs to adjust hedging on the position

In simple terms: An options contract forces the writer to either buy or sell the underlying asset to hedge. The cost of hedging should equal to the option’s premium. The more expensive the hedge, the more the buyer pays for ‘optionality’.

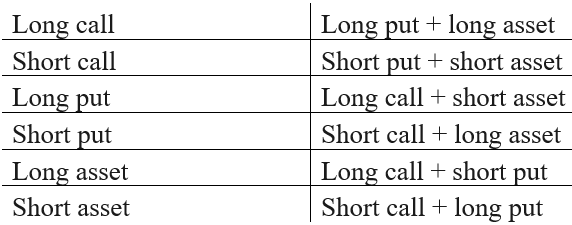

Understanding Put-Call Parity and Synthetics

One of the first things to understand in options is how to price puts in terms of calls and vice versa with a ‘synthetic’ position. This is because any option position (put or call) can be recreated with the opposite option type and a position (long or short) in the asset.

This knowledge will be useful when encountering DeFi protocols which only offer certain types of options. You’ll know how to construct (and compare prices) on the equivalent synthetic structure.

Wong (1991) gives the put-call parity formula as

P = C – S + DF(K)

where

P = put price

C = call price

S = current asset price

K = strike price

DF = discounting function to get the net present value – don’t need to understand this at a basic level

Iguana note: Chief of Maths promises no further equations in this article.

The equation shows that for the same expiration and strike, owning a call option is equivalent to owning the underlying asset and owning a put option. Here is a table of equivalent positions for those who don’t want to check the maths. Options and assets owned are ‘long’ positions. Options written and assets borrowed and sold are ‘short’ positions.

Any option or asset position can be expressed equivalently with a ‘synthetic’ options position. e.g. a long put + the asset is a synthetic version of owning a call.

Put-call parity is the reason why a covered call – commonly touted as an “income” strategy - is equivalent to writing a put. No edge there, just a different way to express the same market exposure.

Implied volatility must therefore be the same for both calls and puts at each expiration and strike. Deviations from this rule represent arbitrage opportunities. Market makers are paid to keep prices in line by arbitraging out violations of put-call parity.

Understanding Option Risks (the Greeks)

*Caution: Turbo Autism detected. Please skip ahead to “Avoiding Rugs” if you wish to avoid.*

The basic definitions are a search engine result away, but we’re adding some color which is harder to stumble upon outside of dense textbooks or industry experience.

Delta - The Rate of Change

Delta risk (also known as the hedge ratio) is the ratio of dollar change in options price to positive dollar change in asset price. An ATM call has a delta of 0.5 and an ATM put has a delta of -0.5. This means an ATM call gains $0.50 in value if the asset increases in value by $1. If 1 option has a quantity of 100 tokens, owning one ATM call has the same delta risk as owning 50 tokens (100 * 0.5). Buying far out of the money call options (low delta, e.g. delta = 10) means that your position will not gain much relative to the gain of the underlying asset (at least while the option is far out of the money).

Gamma - The Rate of Change of Delta

An option’s delta is not constant – gamma describes the sensitivity of delta to a dollar change in asset price. Analogy: delta is velocity, gamma is acceleration. Gamma can be thought of as measuring the added risk to the option from changes in delta. Intuitively, gamma should be highest at the option strike price, as when the market is closer to that price there is greater uncertainty as to whether the option will expire in or out of the money. The owner of an option has positive gamma and the seller has negative gamma.

Theta - Don’t Bleed Out

Theta measures the “time decay” of an option. Theta is the change in the option value per one day change in time remaining to expiration.

In simple terms: all else being equal an option which expires tomorrow will be worth less than an option expiring in a year. More time is your friend.

Intrinsic value is the difference between the asset price and strike price when asset price is above strike for a call and below strike for a put. An option’s premium is calculated by intrinsic value + theta (also known as time value). That means decay is paid by the owner of an option to the writer of an option.

Time decay is not a free lunch - it is compensation for the costs of hedging the option! The options writer is always short gamma meaning he must buy more of the underlying asset as the price rises when short a call and must sell more of the underlying asset as price falls when short a put to stay delta-neutral (hedged). This repetitive ‘buy high and sell low’ behaviour to stay causes trading losses in the asset trades (purchases cost more than the proceeds from sales). In an optimal hedging strategy in a frictionless market (no trading costs) losses from hedging would exactly equal earnings from time decay. Remember this next time you notice someone state that gains from theta are an edge!

The option buyer should be able to extract value from his positive gamma by delta hedging, the reverse of the option writer’s hedging transactions. Zero sum.

Vega - Don’t Get Volatility Rekt

This is one of the most important risks to know – it defines the change in an option’s value for each positive one-point change in the implied volatility. Intuitively an option on a volatile asset (large price swings) is more valuable than an option on a low volatility asset. Markets are usually good at judging the immediate future volatility of a market and this is reflected in the options pricing.

Key takeaway: the implied volatility of an option is forward looking and a good proxy for the market’s overall expectation of how risky (volatile) it is to hold an asset. This can be used as an input when deciding how risky it is to own a stock or a token, see our article on risk.

When implied volatility is higher than recent (historical) volatility, this is a signal to pay attention and look for the cause. Sometimes it can be economic data, earnings releases, clinical trial results, or some other news expected to affect the asset price.

Here is why buying call options on a stock before a potentially positive earnings release seldom results in a profit. Knowledge of an important news release causes relevant options to be priced with higher implied volatility. After the news has been digested by the market and the price has adjusted, the implied volatility reduces.

Losses from vega can offset gains from a favourable price movement, leaving the options purchaser with a net loss. This is especially important for the buyer of calls, especially after a high volatility regime (e.g. a small market crash). ‘Buying the dip’ with call options may not be wise. As the market recovers and volatility calms, the position will lose from vega.

Autist note: trading companies and institutions use the flexibility of options to create superior risk-adjusted returns. Very seldom does this involve taking a directional position only buying a put or call. In the ‘buy the dip’ example, a desk could express their bullish price bias and expectation that volatility would drop by buying the asset and selling 2x the amount of OTM calls, creating a synthetic short straddle above the market price which would benefit both from a rising market towards the strike price and a reduction in implied volatility.

Options buyers always have positive vega (they gain when market expectation of volatility increase and lose when expected volatility falls) and sellers negative vega.

Rho, and other risks

The risk-free interest rate is an important input into the option pricing models, but we need not concern ourselves beyond noting the reality that capital is employed in purchasing an option and this capital has a cost. A discussion of Skew Risk and Lambda, Epsilon, Vanna, Charm, Vomma, Veta, Vera, Speed (DGammaDSpot), Zomma, Color and Ultima is beyond the scope of this article.

This post cannot be a guide on how to trade volatility / options. If you want a turbo deep dive into the maths and practical considerations buy yourself a copy of any of these excellent textbooks:

John Hull: Options, Futures, and Other Derivatives

Sheldon Natenberg: Option Volatility and Pricing

Allen Baird: Option Market Making

Avoiding rugs

If you simply want to understand the space and participate at a small scale without being rugged, avoid these common errors.

1. Selling premium (being short options / short gamma / long theta) is not an edge

Options “educators” (and protocols) promoting selling calls against your holdings often ignore that you’re exposed to the risk of the asset declining in price. This structure is equivalent to writing a put – taking on the risk of being obliged to buy an asset in exchange for a small, fixed premium. If you’re prepared to cap your upside on an asset, it is questionable whether it should be in your portfolio.

Writing calls against your holdings gives up the convexity associated with early tech investing (your investment can only go down 100% but it might return you 300-1,000%+, and in crypto this can take less than a year to see these gains). With a ‘covered call’ option strategy you might cap your gain at 20% in exchange for a modest premium, while still having the risk that your investment in an early stage protocol goes to zero. You need to write calls close to the money to earn any significant premium, which increases your chance of losing out on upside.

Remember that the premium you earn represents the fair cost of hedging your risks in an efficient market. This is not all profit/income, it is compensation for taking risk.

You should be a seller of options if volatility is mispriced (too expensive) either relative to other options/hedges/other exchanges or a proven reliable model of future volatility. Or if a protocol is offering you a generous rebate on losses or other liquidity incentive, which could be considered a form of DeFi yield farming.

Run the maths to make sure staking/farming still makes sense after accounting for risk. No free lunches here, but someone will gladly eat your lunch.

2. Too much theta and too much leverage

Theta (time decay) is not constant and accelerates close to expiration. You should avoid buying short-dated options (unless you have an information edge and your timing is certain) and should close your position before it gets too close to expiry. If the price does not change over time, and implied volatility does not increase, you lose money buying options. A rule of thumb could be choosing an expiration date which is approximately twice the length of your expected hold time.

Note on risk and leverage: options can be a good way to scratch the degen itch responsibly. You can measure your daily loss or gain from theta in any good free options calculator sheet or website. More than 2% of your options degen pot (theta gain or loss per day) suggests you’re overleveraged. This should check you from putting half your portfolio into deep OTM calls which have very little chance of being worth anything at expiry and bleed every day even when the market is rising. Always assume that your option investment will go to zero.

3. The devil is in the details

Markets are fragmented in DeFi options, so you should shop around various protocols to know you are getting a fair price. Compare identical strikes and expiry dates as these affect the price. If the platform quotes IV, use that figure to compare prices easily. You’ll need to do this at the exact moment you execute your trade as prices can chance rapidly - best to have 3 providers side by side in separate browser windows.

Products are often ‘European’ style, exercisable only at expiration. Check if there is a liquid market to sell your options token if you want to close your position before expiration. Point #2 above suggests it is expensive (theta) to hold into expiration, especially if your option is (or could be) near ATM at expiry. And for hedging it is important to understand the contract settlement rules and expiry dates on all products/protocols.

For nearly all people, either staying away from options completely or making a small investment into tokens of protocols they believe will do well is far better than ever trading in puts and calls. The education in this post has a dual purpose: to give information, and to give the reader insight into the complexity of the space (knowing what you don’t know).

Options on DeFi

DeFi has significant pain points onboarding options:

Niche expertise is required to set up an options market making firm. TradFi pays these people very well and locks them up with non-competes, making it difficult for outsiders to bootstrap (as protocols need market makers to provide liquidity)

Complex maths are used to calculate option prices - this is difficult to translate into the solidity language and the Ethereum virtual machine

Formal verification of the mathematics used in options protocols is time consuming and expensive

On-chain computation of prices would be expensive (gas) and until recently there haven’t been good sources for price data which can be pulled from an oracle

Liquidity is extremely thin (chicken and egg problem with demand) and fragmented (across puts/calls, strike prices, expiration dates - easily dozens of distinct option contracts per product)

small cap tokens are probably too illiquid and risky, with small demand for options - the costs of making a market isn’t justified by the revenues, so only BTC and ETH have functioning option markets currently

However, significant progress has been made on all of these points by DeFi pioneers and we look forward to bringing you a protocol deep dive in our next post.

Sources

1) World Federation of Exchanges 2020 market highlights

If you’re reading this and you haven’t subscribed already, join our community of DeFi Turbo Autists!

Until next time, anon..

Disclaimer: None of this is to be deemed legal or financial advice of any kind and the information is provided by a group of anonymous cartoon animals with backgrounds in Wall Street and Software.

Lots of CT buzz about dopex. I know nothing. I’m a simple ape on the finance stuff. But they have a token, wen defieducation article

Super interesting topic, thank you!

I know enough about options to not use them in crypto (don't think I have an edge and afraid of low liquidity) but the topic is fascinating (looking forward to your view on PERP also).

Some questions if you don't mind :

1. Is there a VIX equivalent in crypto or ways to evaluate vol?

2. Is there the equivalent of implied vol and realized vol for each contract? (and does the trading platoforms show it?)

3. Is there equivalent of LEAPS? How is the liquidity on those?

4. I was going to ask wich tokens of protocols you analyse as the best in this field but it sems you'll cover that in next posts?